The Global Financial Centres Index

Methodology

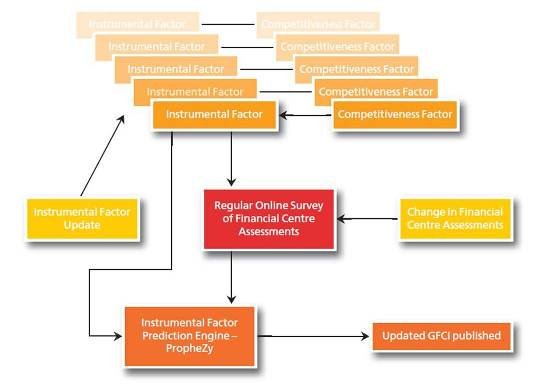

The GFCI provides ratings for financial centres calculated by a ‘factor assessment model’ that uses two distinct sets of input:

- Instrumental Factors: objective evidence of competitiveness was sought from a wide variety of comparable sources. Click here for details. For example, evidence about the telecommunications infrastructure competitiveness of a financial centre is drawn from the ICT Development Index (supplied by the United Nations), the Networked Readiness Index (supplied by the World Economic Forum), the Telecommunication Infrastructure Index (by the United Nations) and the Web Index (supplied by the World Wide Web Foundation). Evidence about a business-friendly regulatory environment is drawn from the Government Effectiveness rating (supplied by the World Bank) and the Corruption Perceptions Index (supplied by Transparency International) amongst others. A total of 145 instrumental factors are used in GFCI 35 (of which 49 were updated since GFCI 34 and 2 were new to the GFCI). Not all financial centres are represented in all the external sources, and the statistical model takes account of these gaps.

- Financial Centre Assessments: by means of an online questionnaire, running continuously since 2007. We used 48,365 financial centre assessments drawn from 8,494 responses in GFCI 35.

Financial centres are added to the GFCI questionnaire when they receive five or more mentions in the online questionnaire in response to the question: “Are there any financial centres that might become significantly more important over the next 2 to 3 years?” A centre is only given a GFCI rating and ranking if it receives more than 150 assessments from other centres within the previous 24 months in the online survey. Centres in the GFCI that do not receive 50 assessments in a 24 month period are removed and added to the Associate list until the number of assessments increases.

At the beginning of our work on the GFCI, a number of guidelines were set out. Additional Instrumental Factors are added to the GFCI model when relevant and meaningful ones are discovered:

- Indices should come from a reputable body and be derived by a sound methodology;

- Indices should be readily available (ideally in the public domain) and be regularly updated;

- Updates to the indices are collected and collated every six months;

- No weightings are applied to indices;

- Indices are entered into the GFCI model as directly as possible, whether this is a rank, a derived score, a value, a distribution around a mean or a distribution around a benchmark;

- If a factor is at a national level, the score will be used for all centres in that country; nation-based factors will be avoided if financial centre (city)-based factors are available;

- If an index has multiple values for a city or nation, the most relevant value is used (and the method for judging relevance is noted);

- If an index is at a regional level, the most relevant allocation of scores to each centre is made (and the method for judging relevance is noted);

- If an index does not contain a value for a particular city, a blank is entered against that centre (no average or mean is used).

Creating the GFCI does not involve totaling or averaging scores across instrumental factors. An approach involving totalling and averaging would involve a number of difficulties:

- Indices are published in a variety of different forms: an average or base point of 100 with scores above and below this; a simple ranking; actual values (e.g. $ per square foot of occupancy costs); a composite ‘score’;

- Indices would have to be normalised, e.g. in some indices a high score is positive while in others a low score is positive;

- Not all centres are included in all indices;

- The indices would have to be weighted.

The guidelines for financial centre assessments by respondents are:

- Responses are collected via an online questionnaire which runs continuously. A link to this questionnaire is emailed to the target list of respondents at regular intervals and other interested parties can fill this in by following the link given in the GFCI publications;

- Financial centre assessments will be included in the GFCI model for 24 months after they have been received;

- Respondents rating fewer than 3 or more than half of the centres are excluded from the model;

- Respondents who do not say where they work are excluded;

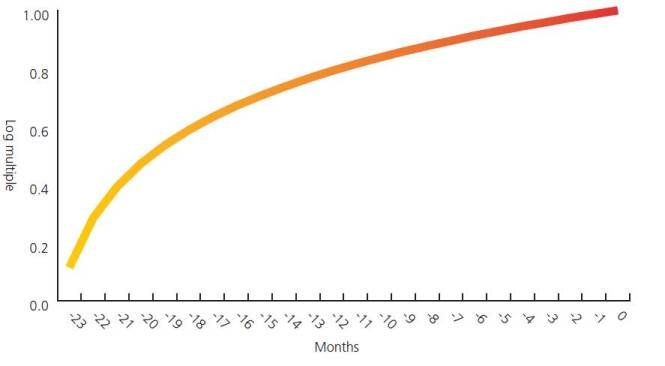

- Financial centre assessments from the month when the GFCI is created are given full weighting and earlier responses are given a reduced weighting on a log scale.

The financial centre assessments and instrumental factors are used to build a predictive model of centre competitiveness using a support vector machine (SVM). SVMs are based upon statistical techniques that classify and model complex historic data in order to make predictions on new data. SVMs work well on discrete, categorical data but also handle continuous numerical or time series data. The SVM used for the GFCI provides information about the confidence with which each specific classification is made and the likelihood of other possible classifications.

A factor assessment model is built using the centre assessments from responses to the online questionnaire. Assessments from respondents’ home centres are excluded from the factor assessment model to remove home bias. The model then predicts how respondents would have assessed centres with which they are unfamiliar by answering questions such as:

If an investment banker gives Singapore and Sydney certain assessments then, based on the instrumental factors for Singapore, Sydney and Paris, how would that person assess Paris?

Or

If a pension fund manager gives Edinburgh and Munich a certain assessment then, based on the instrumental factors for Edinburgh, Munich and Zurich, how would that person assess Zurich?

Financial centre predictions from the SVM are re-combined with actual financial centre assessments (except those from the respondents’ home centres) to produce the GFCI – a set of financial centre ratings. The GFCI is dynamically updated either by updating and adding to the instrumental factors or through new financial centre assessments. These updates permit, for instance, a recently changed index of rental costs to affect the competitiveness rating of the centres.

The process of creating the GFCI is outlined diagrammatically below:

It is worth drawing attention to a few consequences of basing the GFCI on instrumental factors and questionnaire responses:

- Several indices can be used for each competitive factor;

- A strong international group of ‘raters’ has developed as the GFCI progresses;

- Sector-specific ratings are available using the business sectors represented by questionnaire respondents. This makes it possible to rate London as competitive in Insurance (for instance) while less competitive in Investment Management (for instance).

- The factor assessment model can be queried in a ‘what if’ mode - “how much would London rental costs need to fall in order to increase London’s ranking against New York?”

Part of the process of building the GFCI is extensive sensitivity testing to changes in factors of competitiveness and financial centre assessments. There are over ten million data points in the current model. The accuracy of predictions given by the SVM are regularly tested against actual assessments.