Policy Performance Bonds For ESG & Climate Change – A Primer

Monday, 01 July 2019By Professor Michael Mainelli

Governments and companies often make promises they can’t or won’t keep. From enhancing educational attainment, to reducing unemployment and cleaning up air and water, governments make promises by setting policies. Equally, governments announce policies designed to get companies to invest, companies often make substantial commitments to the future on behalf of wider society.

People depend on such promises to understand intentions, allocate resources, or prioritise support. When promises aren’t kept, people are confused, poorer, and warier.

However, whilst people from President Obama to Sir Nicholas Stern to the musician Bono have called for investment in low carbon technologies to rescue us from the consequences of climate change, rhetoric has often failed to live up to reality.

The scale of the investment required is not always appreciated. In their ‘beyond alternative’ or ‘blue scenario’ the International Energy Agency begin to map out the investment needed for renewables to really transform the outlook for energy and climate in the mid 21st century.

In 2010 the IEA estimated that to achieve this transformation and keep global temperature rises below 2 degrees, hundreds if not thousands of gigawatts from low carbon sources were required. This happens to be in line with the London Accord bottom up estimates and the Stern Review’s ball park figure of 1% of global GDP from 2007.

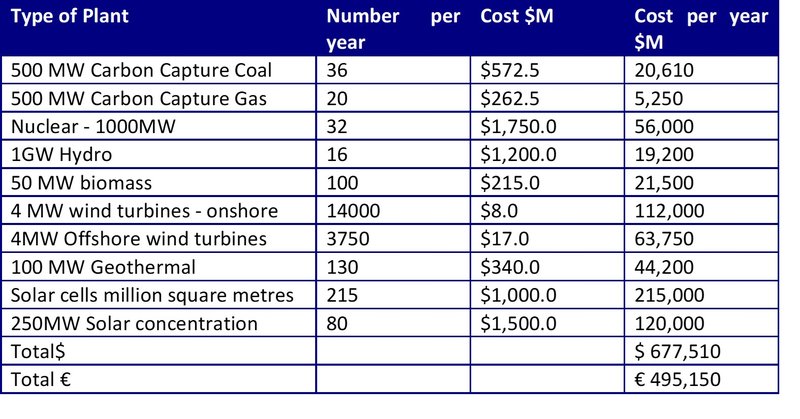

This represents an annual installation of some 50 carbon capture thermal plants, 30 nuclear plants, 17,000 on and off-shore wind turbines, 100 biomass plants, 130 geothermal schemes, 80 solar concentration plants, 16 GW of hydro schemes, and 200 million square metres of solar cells: a simple estimate of the cost of this quickly reaches some €500 billion a year. Whilst progress is accelerating, and the costs of certain technologies, such as photovoltaics has fallen, in 2015 the shortfall in investment was $171 billion .

Table 1 Required Annual Investment in Low Carbon Energy Generation

Source London Accord “A Portfolio Approach To Climate Change Investment And Policy”

Investment of this scale cannot come from the public sector alone, private sector investment is required on a truly global scale. However, potential climate change investors have one big doubt – are governments truly committed to decarbonising the economy?

All energy projects share similar risks. Universal risks include energy prices, construction costs, operating costs, efficiency, waste and decommissioning. But there is one qualitative difference between traditional fossil fuel energy projects and nuclear or clean tech energy projects, the risk of failed government policy.

Developers of low carbon projects, such as wind farms or solar companies, face two major problems turning ideas into reality. The first is showing attractive returns. The second is raising capital. Most low carbon projects will provide attractive returns only if government policies allow a level playing field with fossil fuel power generation- not only in terms of hidden subsidies such as tax breaks, but also in terms of allowing access to power networks by controlling connection costs. Over the long term these should not only lead to lower emissions, but to higher fossil fuel prices and higher carbon prices.

Unfortunately, policy commitments on tackling climate change can wither like spring blossoms in late frost, in the face of democratic regime change, or even mid-term if a government feels that its popularity is wavering. Uncertainty about government commitments creates risks which developers, and their investors, are not keen to bear.

On the world stage governments claim they are committed, but history raises doubts about their sincerity. Repeated changes of policy on feed-in tariffs for solar power generation in Spain and Germany, a moratorium on on-shore wind power generation in the England and a dysfunctional relationship with nuclear power across Europe bear witness to millions of pounds of wasted professional fees and damaged investments by private companies in a low carbon future.

Unfortunately, Government policy is essential to most clean tech profitability. If governments stick to declared targets for reducing greenhouse gas emissions, renewable energy, or carbon prices, many clean tech projects make investment sense however, if governments are blowing so much hot air, clean tech projects are highly risky. This risk, the risk of government inaction, has significant financial implications as it drives up the cost of finance for clean energy substantially.

Lack of confidence in government commitment impairs investment. Lack of confidence also leads to low prices for carbon. For example, the EU ETS market Phase 1 (2005 to 2007) carbon price crashed in 2007 when it became apparent that EU governments had jointly issued far too many permits to emit, i.e. clearly they weren’t committed to reductions. The uncertainty about government commitment manifests itself in three specific risks – government carbon emission targets being missed, fossil fuel prices remaining low, and carbon (emissions) prices remaining low. Missed targets, low fossil fuel prices and low carbon prices reduce the profitability of clean energy, or cause losses.

How Can These Risks Be Hedged?

Sovereign Carbon Bonds, a type of Environmental Impact Bond, could provide an important link between government policies and companies as they would help unite businesses, organizations, and governments towards shared goals. Such instruments could provide the necessary link between macroeconomic incentives and microeconomic insurance opportunities that are key to achieve the two degree scenario.

Environmental Impact Bonds (EIBs) are government bonds where interest payments are linked to the delivery of an environmental policy specific target. If a target is missed, the yield on the bond increases. In other words policy makers will be held to their promises, and if they fail to deliver there will be a financial penalty. An EIB provides a hedge against the issuing country’s government not delivering on its commitments or targets and could help unite businesses, organizations, and governments towards shared goals.

Environmental Impact Bonds And The Paris Agreement

At the Paris climate conference (COP21) in December 2015, 195 countries adopted the first-ever universal, legally binding global climate deal.

The agreement, which sets out a global action plan to put the world on track to avoid dangerous climate change by limiting global warming to well below 2°C, is due to enter into force in 2020.

Before and during the Paris conference, countries submitted Intended Nationally Determined Contributions (INDCs). INDCs are comprehensive national climate action plans and are the primary means for governments to communicate internationally the steps they will take to address climate change in their own countries. INDCs reflect each country’s ambition for reducing emissions, taking into account its domestic circumstances and capabilities. Some countries also address how they’ll adapt to climate change impacts, and what support they need from, or will provide to, other countries to adopt low-carbon pathways and to build climate resilience.

Carbon Policy Performance Bonds (OAT CPBs) are a simple, and yet powerful idea that could provide a framework for the delivery of INDCs. In its simplest form, interest payments could be linked to the actual greenhouse gas emissions of the issuing country against the targets contained in its INDC. An investor in this bond receives an excess return if the issuing country’s emissions are above the government’s published target.

OAT CPBs could be designed against a variety of indices to track performance including -

- Levels of greenhouse gas emissions;

- Levels of feed-in tariffs for renewable energy;

- Percentage of renewable energy in overall energy supply;

- Prices of emission (reduction) certificates in a trading system;

- Levels of taxes on fossil fuels or fossil fuel end-user prices.

The choice of index allows the public sector to eliminate quite specific risks and so, akin to a surgical strike, take out a policy confidence blockage and enable private sector investment to flow. The ability to choose any of a range of indices provides flexibility to target one or more specific risks in a single structure. OAT CPBs could easily be issued by any government (supra-national, national, state, province) or multi-lateral agency without any need for a global initiative. Documentation would be simple (please refer to the appendix for a term sheet example).

Most existing government treasury mandates already allow for these types of instrument. For example inflation indexed bonds are bonds where the principal is indexed to inflation or deflation on a daily basis. They are thus designed to hedge the inflation risk of a bond. The first known inflation-indexed bond was issued by the Massachusetts Bay Company in 1780 The market has grown dramatically since the British government began issuing inflation-linked Gilts in 1981. As of 2008, government-issued inflation-linked bonds comprise over $1.5 trillion of the international debt market .

Hedging And Derivatives

The ability to hedge would enable investors to invest more confidently in projects or technologies that pay off in a low-carbon future because if the low-carbon future fails to arrive the government too bears direct costs of having to pay higher interest rates on government debt. In this way, OAT CPBs eliminate the one risk that differentiates clean tech projects from other energy projects, the uncertainty of government policy actually being directed at a low carbon future.

Eventually, if the bonds are actively traded, simple derivatives would allow potential investors in low carbon projects or technologies to obtain a hedge against government risk without having to physically purchase the government bond itself.

Derivatives would broaden the appeal to investors prohibited from buying government debt, for example those whose investment mandate stipulates they must invest in low carbon projects only.

More complex versions are possible. A developed country could issue the bond, but use an index of a group of developing countries weighted average feed-in tariffs for clean energy, for example, so transferring the risk of those governments’ policies from a private sector investor to the developed country’s government.

Climate

Mark Carney, Governor of the Bank of England and Chair of the Financial Stability Board, stated in a lecture in Berlin on 22 September 2016 :

“.... green finance is a major opportunity. By ensuring that capital flows finance long-term projects in countries where growth is most carbon intensive, financial stability can be promoted. By absorbing excess global saving, equilibrium interest rates can be raised and macroeconomic stability enhanced. And by allocating capital to green technologies, the prospects for an environmentally sustainable recovery in global growth will increase … the more we invest with foresight; the less we will regret in hindsight. Financial stability risks will be minimised if the transition begins early and follows a predictable path, thereby helping the market anticipate the transition to a two-degree world.”

He continued:

“The development of this new global asset class (green bonds) is an opportunity to advance a low carbon future while raising global investment and spurring growth ... The shift to the capital markets from banks will also free up limited bank balance sheet capacity for early-stage project financing and other important infrastructure lending.

To reach escape velocity, (green bond) market participants and public authorities will need to coordinate to deliver common green bond frameworks and definitions, and other necessary supporting infrastructure, to build local and cross-border markets.

Specific measures could include:

- Developing a ‘term sheet' of internationally recognised standardised terms and conditions for a green bond. ..... This should significantly improve the ease and efficiency of green bond issuance and simplify investor access to green bond markets in multiple currencies, thereby moving them into the mainstream of finance.

- Creating voluntary definitional frameworks, certification and validation to give certainty to issuers and investors that the project being financed is ‘green'.

- Developing green bond indices to unlock the potential investment power of passively managed investment

- Assessing the scope for standardisation and harmonisation of principles for green bond listings to promote efficient trading and adequate liquidity.”

Have An Issue? We Have A Bond For That!

OAT CPBs could provide a hedge against an issuing country’s government not delivering on its commitments or targets whatever they may be. Thus they could be issued in any area where policy risk is significant, particularly those where politicians wish to encourage private sector engagement. Policy areas where OAT CPBs could be issued include flooding, education, health, wildlife protection, reforestation, inflation, or unemployment.

The ability to hedge enables the same investor to invest more confidently in projects or services that deliver against policy goals, because if the government fails to follow through it will bear direct costs of having to pay higher interest rates on government debt. In fact, a small exercise using the UN Sustainable Development Goals as a template easily inspired OAT CPBs for every category:

- poverty elimination

- unemployment bonds

- minimum household income bonds - food security and improvement

-nutritional supplement bonds

-import percentage bonds - population health

-antibiotic resistance bonds

-obesity bonds

-drug use bonds - educational attainment

-apprenticeship bonds

-PISA bonds - gender equality

-female educational attainment bonds

-quota target bonds - water

-flood bonds

-water purity and availability bonds - energy

-alternative energy percentage bonds

-energy delivery bonds - economic growth

-GDP bonds

-export value-added bonds - infrastructure

-road network bonds

-broadband coverage bonds - inequality

-maternity death bonds

-GINI index bonds - city safety and sustainability

-crime reduction bonds

-air quality bonds - sustainable consumption and production

-recycling target bonds

-biomass bonds - climate change

-CO2 emission bonds

-CO2 sequestration bonds - oceans and seas

-fish stock quality bonds

-desalination bonds - forestry and land use

-forestry coverage bonds

-pesticide consumption bonds - inclusive societies and institutions

-corruption index bonds

-court case time bonds

Why Are Policy Performance Bonds Such Powerful Instruments?

In finance, a bond is an instrument of indebtedness of the bond issuer to the holders. They are debt securities under which the issuer owes the holders a debt and, depending on the terms of the bond, is obliged to pay them interest (the coupon) and/or to repay the principal at a later date, termed the maturity date.

The Latin motto of the London Stock Exchange is ‘Dictum Meum Pactum’ or "My Word is My Bond." Unfortunately the promises of policy markets have never been bankable.

By issuing policy performance bonds linked to independent, auditable indices, these ‘bond cuffs’ would directly address the primary concern of private sector investors, lack of confidence in governments’ commitments.

For example - In the UK, analysts claim that retail banking is dysfunctional and systemically dangerous because an oligopoly of five retail banks controls 85% of the market. The UK government claims its policies include support for new ‘challenger’ banks.

If it’s serious, the UK government could issue a PPB stating perhaps that it would aim for the oligopoly to have less than a 50% market share by 2025. That would show firm commitment.

Investors in challenger banks could hedge the risk that future banking regulation would harm their investments by buying such bonds. If the oligopoly were still as strong, the investors would have had some recompense from government. If the oligopoly was weaker, presumable the challenger banks would have done well, and those investors who hedged would have paid the government for their hedge by lending government money at lower rates over that decade. Policy performance bonds could be structured to tackle excessive credit growth, measure effective regulation, or increase non-leveraged home rental markets.

Consequently, changes of policy which disadvantage investors in renewable energy investment, can be hedged using OAT CPBs- as the government would be forced to increase interest rates if it failed to reach its CO2 reduction targets, or its targets with regards to GWh of clean energy generation.

The Liquidity Of Bond Markets

Following the financial crisis of 2007 -2009 banks were hit by a wave of regulations in the area of governance, market infrastructure, disclosure and capitalisation. Basel III enhanced capital and liquidity requirements, whilst the US Federal Reserve’s Dodd-Frank Wall Street Reserve and Consumer Protection Act and Volker Rule prohibited Banks from engaging in short term proprietary trading.

The impact of these regulator strictures has been to increase costs for banks and reduce their ability to support credit growth and economic recovery .

The two traditional routes available to corporations seeking capital are issuing shares or issuing corporate bonds. Corporate bond markets are an essential part of capital markets as they bring together businesses who require capital with investors and savers who wish to earn a stable income from their investments and savings.

Bonds play a key role in facilitating economic growth, productivity, and employment. As the ability of banks to provide direct funding to the corporate sector has become challenged, post-crisis, policy makers are beginning to look to capital markets as an ever more important source of financing for the real economy, while also underpinning economic stability.

However, recently concerns have been expressed about liquidity in the corporate bond market. (A market for a security is considered liquid if investors can trade it – even in large size – at low cost, because their orders have little effect on its price). This matters because any decline in the liquidity of bonds could make it more expensive for borrowers to issue them in the first place, and this could hurt investment and economic growth.

Whilst the bond market has doubled in size in the past decade, at the same time, banks - the market-makers for these assets, or traditional shop front - have cut their holdings. The Bank of England estimates there has been a 75% reduction in the bond inventories of dealers in the marketplace since 2008 , fuelled by dealers reluctance to trade corporate bonds and other fixed-income securities due to additional costs of holding them on their balance sheets.

This means that buying or selling bonds could become harder, which could in turn lead to larger pricing swings. One possible solution to this problem (in addition to modernising trading infrastructure), is diversifying the range of bonds that can be purchased.

Expecting The Unexpected - Policy Default Swaps

A credit default swap (or CDS) is an insurance policy, or protection, against default on a debt. The seller of a CDS is effectively ‘selling protection’, and will pay the buyer of the CDS (who is ‘buying protection’) an agreed amount in the event of a default, or ‘credit event’, of the debtor (i.e. the corporation, bank, or state against which the CDS is written).

Credit events are usually a failure of the debtor to make payment on its debt (either loans or bonds), but can also include restructuring or bankruptcy (the definition of a ‘credit event’ is written into the terms of the contract). The buyer of CDS pays an annualized premium to the seller over the life of the CDS in return for this protection.

The premium paid for a CDS can be viewed as the probability of a credit event over the life of the CDS contract. Recently, there has been an attempt to make CDS more standardized, and more ‘bond like’ in their structure. For instance, CDS contracts tend to have standardized maturities (such as 3yr, 5yr, 7yr, and 10yrs, with 5yrs being the most popular), standardized contract dates (quarterly) and roll-dates (semi-annual), and even coupons (in Europe this is 1% for IG and 5% for HY).

A Policy Default Swap would be similar in structure to a CDS but could indemnify a company or Government against losses incurred as a result of a “Policy Event” preventing it from attaining the targets set in a policy performance bond. Policy events could include changes in public policy resulting from a general election or natural disasters.

Policy Performance Bonds - Something To Keep Everyone Happy?

- Central Bankers - In the financial crisis, central banks acted as market makers of last resort by pumping money into the economy through quantitative easing (QE)- buying assets, usually government bonds, from investors such as banks or pension funds, with money they had "printed" - or, more accurately, created electronically. The aim of QE is to increase the overall amount of useable funds in the financial system. However, in August of this year, when, in attempt to stimulate the UK economy following the Brexit vote, the Bank of England embarked on a new round of quantitative easing it faced difficulties.

The Bank fell £52m short of its £1.17bn target when it failed to find enough sellers. That drove up prices and pushed down yields, to investors. As a result on the morning of Wednesday 10th August UK Government bonds (GILTs) maturing in 2019 and 2020 were yielding minus 0.1%. If Governments were to enhance the range of sovereign bonds on offer by issuing PPB, the task of central banks would be made easier and volatility in the bond markets would be reduced.

Furthermore, central banks around the world are increasingly concerned about the impacts of climate change on the long-term performance of country economies- a recent article in Nature estimates that climate change could cut the value of the world’s financial assets by $2.5tn. Central banks should welcome Carbon PPBs as concrete evidence that governments are serious in their attempts to avert catastrophic climate change. - Central Governments - Due to the credit crunch the IMF estimates that G10 governments are likely to issue trillions in bonds over the next few years. With so much planned debt issuance, governments need ways to distinguish themselves in a crowded bond market. Just as governments fought to issue inflation linked bonds when their inflationary risk dominated, they can now issue policy performance bonds when government inaction or commitment risk dominates.

- Insurers -As major players in the primary bond markets insurers stand to gain from the issuance of PPB. Firstly PPBs would enable them to diversify their holdings, and secondly as insurers are in the front line to take a hit from climate change fuelled natural disasters, Climate Policy Bonds would hedge their risk exposure to increased damage due any policy changes which are detrimental to the climate.

- Accountants and Auditors - Accountants would have a central role in determining the validity of metrics associated with corporate policy bonds and analysing the impact of increased or decreased costs of borrowing associated with corporate policy bond performance. National auditing agencies would be responsible for holding governments to account.

- Credit Rating Agencies - Would be able to accurately assess the credit risk of corporate and government borrowers with respect to policy performance bonds, based on the reality gap between politicians’ rhetoric and national statistics.

- Investment Managers and Pension Funds - Traditionally, over the long term (ten years or so) equities have been seen as a better investment as their yield is higher. This is why pension funds generally invested in equities. However in recent years there has been a significant change in the investment profiles of pension funds, which for the first time in decades now hold more bonds than stocks . By increasing their holdings of long-term bonds, funds can more closely match their returns to their future commitments, limiting the volatility of their pension obligations and locking in gains. However, this demand for highly rated debt issues is pushing up prices and driving down yields. Diversification into PPBs could stablilise both prices and yields.

- Stock Exchanges and Trading Platforms - Unlike equities, the secondary market for bonds is relatively small and the majority are currently traded over the counter (OTC). The primary reason for this is their diversity (differing issuers and issues with differing maturity rates and yields). As PPBs could be classed according to the policy they are linked to, the development of a common trading platform would be easier, thus assisting in the development of a secondary market.

- Companies and Investors - The ability to hedge major investments in infrastructure, such as renewable energy plants or services, such as education would provide a level of security for corporations seeking to deliver goods and services designed to enhance environmental or social conditions.

- The Public - “People only accept change when they are faced with necessity and only recognise necessity when a crisis is upon them,” said Jean Monnet, the French political economist whom many consider to be the founding father of the project of European integration. The slow pace of climate change, punctuated by an increasing tempo of extreme event, means that public consciousness has not yet recognised global warming as a crisis. However concrete action by politicians epitomised by policy performance bonds will assist the public to accept the inevitable changes to national infrastructure, attitudes to energy use and lifestyles that effective action on climate change will require.

- Politicians - Whilst at first glance there seems to be little incentive for politicians to willingly shackle themselves to their promises, the issuance of PPB would serve a number of purposes. Firstly at a time when the public’s belief in politicians and the political process is at an all time low, the issuance of PPBs would be a gold standard for trust. Secondly, as policy reversals would have a financial impact on the government, political legacies would be somewhat protected from democratic changes of government. Finally, as the issuance of PPBs would be carefully watched by both treasuries and central banks, a more consensual, evidence based style of policy making would be encouraged.

When Will The First Policy Performance Bond be Issued?

The concept of policy performance bonds was first formally presented by Z/Yen at the World Bank Government Borrowers' Forum in Ljubljana in May 2009. Since 2009 there have been numerous discussions with national governments, central banks, debt offices, and a number of entrepreneurial national and state governments. Pension funds are particularly interested in using them to hedge government policy risk. One large pension fund stated to a UK minister, “if you issued these policy performance bonds for renewable energy, we’d buy them tomorrow morning, Minister”.

The City of London put forward the idea in its climate change form in its 2009 Copenhagen COP submission. UNA put the idea into its 2015 Paris COP submission too.

There are certainly complexities in the issuance of this type of bond, such as auditing and authentication of government figures, liquidity, leverage opportunities, stripping, etc., but these are relatively easily overcome.

However, the biggest challenge to overcome with respect to the development and issuance of policy performance bonds is political.

The long term nature of bonds (with typical maturities of more than 10 years) would require policy stability across parliamentary cycles. A consensus based process for agreeing goals would require a more grown-up style of politics than has been common in recent years, one would be based on evidence based policy.

This may be difficult at a national level however, there may be scope to develop these instruments at a sub-regional or city level. Municipal bonds are commonly traded in the United States where more than $3.7 billion of ‘munis’ have been issued Whilst munis are rarer in Europe, national governments may wish to trial Policy Performance Bonds at a city level before issuing OAT CPBs or other types of PPBs as sovereign gilts.

However, the biggest drawback is that governments would actually have to pay if they change policy, or do not enact promised policies and as yet no government has had the courage to back its rhetoric with the cast iron guarantee of a policy performance bond.

Much more information on Policy Performance Bonds.

Bond Term Sheets

Typical term sheets might be explored here:

http://azurekingfisher.com/media/upload/tier_ii_termsheet_students.pdf

But let’s flesh out two examples of policy performance bonds.

Example 1 - Government Carbon Policy Performance Bonds

An attractive option would be for project developers to issue bonds indexed to the three key risks – government performance against targets, fossil fuel prices against a break-even level, and carbon prices against a break-even level? Such policy performance bond would reduce the cost of capital for a developer exactly in those situations where the profitability of clean energy is threatened by government action, or inaction.

Bonds indexed to emissions, fossil fuel prices or carbon prices would transfer the risk from the developer to the investor. But we know that investors are not keen to bear those risks, either, from their reluctance to fund many clean energy projects. Investors cannot easily hedge those risks, but that is exactly where government can help – by issuing debt with the opposite risk profile. Government carbon policy performance bonds would provide greater returns if government falls short of achieving its targets, if fossil fuel prices remain low, or if carbon prices remain low. That kind of index-linked OAT could easily be issued, and it would provide a natural hedge against our project developers’ government risk. An investor would invest in a low carbon project (either equity or debt), and simultaneously buy a proportion of index-linked government carbon bonds.

As an example, take an investor looking at investing in a 2010 wind farm that is competitive at £55/megawatt-hour. Say that the price of fossil fuel derived power is £50/megawatt-hour in 2010, with a government target of £75/megawatt hour in 2015.

The index-linked OAT to provide a hedge would pay a margin over normal OATs, with the margin a function of the fossil-fuel derived power price. For example, for every £1 below £75, the interest rate could go up by 1%, with a suitable cap at say 20%. For every £1 that the fossil-fuel derived power price is above £75, the interest would reduce by 1% with a minimum of zero. An investor in such OATs would be able to offset the price risk of his or her investment in the wind farm.

Other structures are possible, too, linking the principal repayment to fossil fuel prices, or either interest rate or principal to actual emissions in, say, 2020.

As a simple example, take an investor looking at investing in a 2010 wind farm that is competitive at €95/megawatt-hour. Say that the price of fossil fuel derived power is €70/megawatt-hour in 2010, with a government target of €105/megawatt hour in 2015. The index-linked OAT to provide a hedge would pay a margin, with the margin a function of the fossil-fuel derived power price. For example, for every €5 below €105, the interest rate could go up by 1%. For every €5 that the fossil-fuel derived power price is above €75, the interest would reduce by 1% with a minimum of zero. A creative borrower might offer leveraged products where the interest rates changed at different rates above or below the target. The benefit to the investor in such bonds (OATs) would be able to offset the price risk of his or her investment in the wind farm.

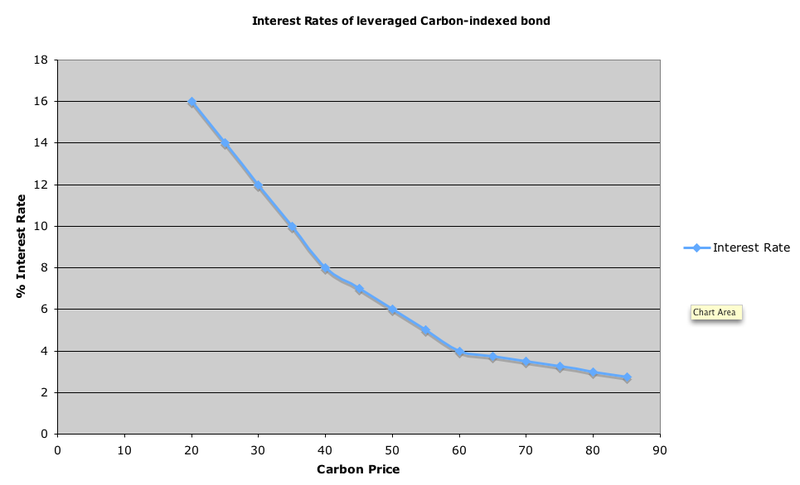

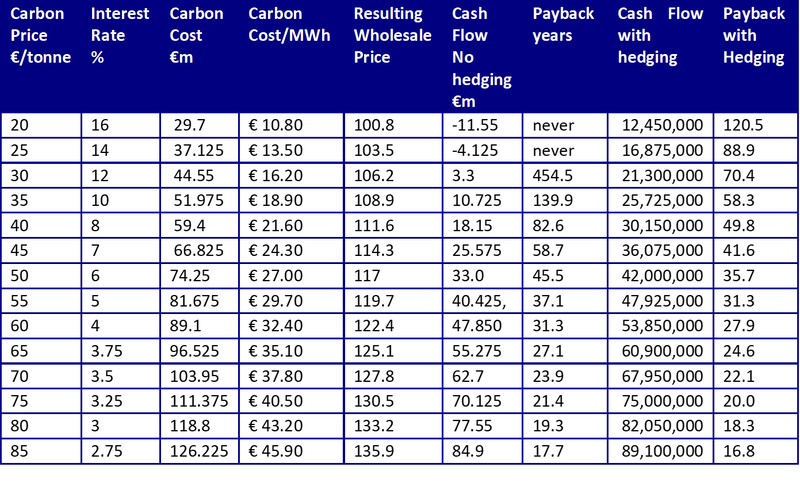

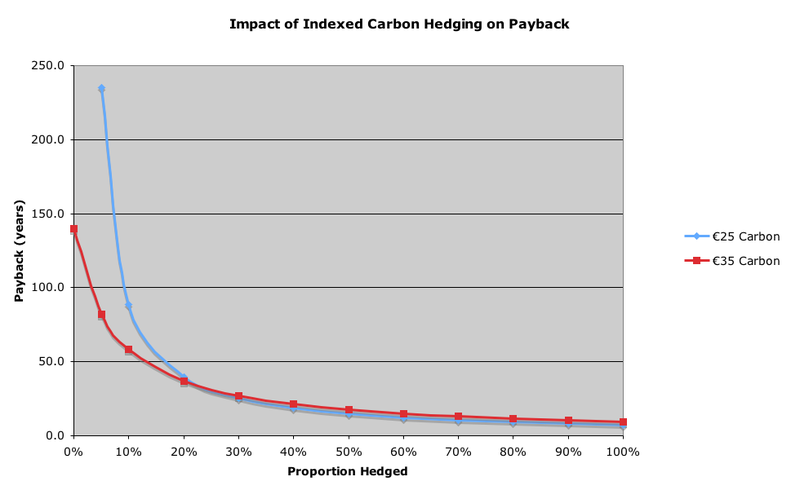

An example of a more complex investment where a carbon index instrument could help considerably, one might take a tidal barrage scheme. Such schemes have characteristically huge capital costs, low costs of operation once installed, and long lifetimes (around 200 years). This means they are difficult to value using conventional discounted cash flow methods. In Index A we show some calculations for a 4 km barrage costing €1.5bn (and some will be 10-20 times larger) producing 2.75 terawatt hours of electricity per year. This scheme needs carbon prices of €40/tonne CO2e to give a payback period around 80 years and a price of €60/tonne for a payback of 30 years. (Carbon prices raise the wholesale costs of electricity produced by conventional means, thus increasing the price that we could charge from the barrage scheme). We show the effect of the investor buying a bond paying 4% index to a carbon price of €60/tonne. The bond is leveraged – above €60, the interest rate falls by 1% for every €20 increase in carbon. Below €60 the interest rate increases by 1% for every €5 decrease in the carbon price, and below €40 the rate increases by 1% for every €2.5 decrease. Here is a graphic of the interest rate structure:

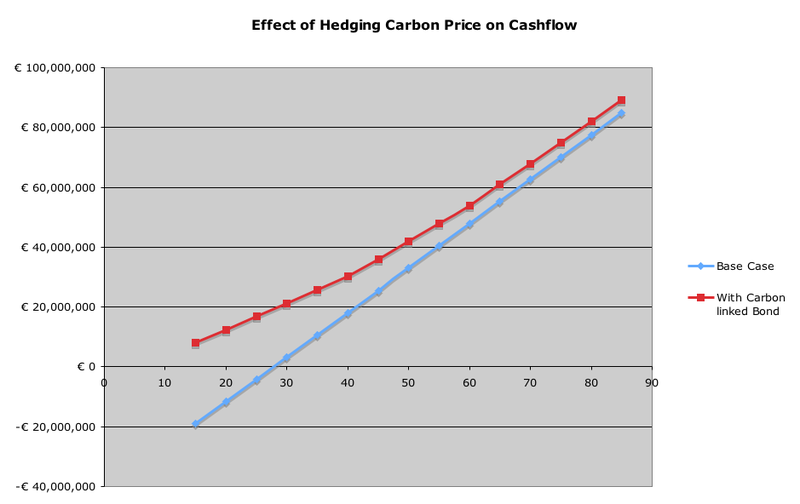

The impact of such an instrument is to significantly reduce the investors’ carbon price risk. Interestingly, the investor does not have to hedge the entire capital sum of €1.5billion. Buying bonds of 10% of the project capital (€150m) is sufficient in this case to hedge against a fall in the carbon price to €30/tonne.

Without the bond the payback period for the project is 450 years (longer than its expected lifetime), while with the bond its payback is 70 years.

As an example, hedging a large renewables project with a capital cost of €1.5bn that produces 2.75 terawatt hours of electricity per year is set out below. The plant produces electricity at a cost of €105/MWh, and the wholesale price of electricity without carbon pricing is assumed to be €90/MWh. The table shows payback periods with and without ‘hedging’ (buying a leveraged 4% bond linked to the price of carbon emissions permits (probably those traded on the EU/ETS). In this case the amount hedged is 10% of the total capital cost or €150m.

An alternative hedging approach would be for the project investor to enter into a “carbon swap.” The terms of such a swap would have the investor pay a fixed rate of interest on the notional amount of the swap, and receive a payment based on the difference between the spot carbon price on a payment date and an agreed upon floor. The swap market makers would still require the government to issue the index-linked OATs (the net effect off the swap would be to create synthetic fixed rate OAT) until such time when a forward market in carbon developed, similar to the LIBOR futures market.

The advantages of a swap scheme for investors would include, no additional capital outlays for a hedge if the swap were struck “at the market”, with a product whose existing regulatory framework mitigates counterparty risk (notwithstanding today’s headlines). Large participants in mortgages markets already use swaps in a similar way to hedge prepayment risk on fixed rate mortgages by entering into fixed/floating interest rate swaps. The long effective duration of the swap provides an efficient tool to manage the negative convexity inherent in fixed rate prepayable mortgages.

Other structures are possible, too, linking the principal repayment itself to emissions, fossil fuel prices or carbon prices, or perhaps feed-in tariffs. Maturity dates, structures and tranches can all be varied. One objection to index-linked carbon OATs is that governments do not control emissions as they do inflation. True, but governments may have as much control. Emissions are at least as much under government control as inflation, which is subject to import/export ratios, money supply, credit, productivity, weather and all the vagaries of an economy. Secondly, in multi-government emissions, such as the European ETS, a quick comparison with the European Central Bank on inflation shows that governments have a similar amount of joint control on emissions.

One quick observation is that if people are investing in OATs as well as green or clean tech investments, the investment pool for green tech has shrunk. Strictly, this may be true, but half of something is better than all of nothing. In fact, if people truly believe governments will meet their emission goals, then the index-linked bonds will fall in value and investors will not need to use them in green tech investment, thus all desired investment would be directed at green tech. Moreover, investors, such as insurers and pension funds, are investing on a portfolio basis. Their ability to hedge government risk of non-performance in their portfolio is likely to increase their low carbon holdings markedly.

Another observation is that index-linked carbon OATs would be more effective with more leverage, i.e. being more geared with payouts as multiples compared with typical amounts of principal funding. The leverage behind index-linked carbon OATs could be increased if governments wanted simply by leveraging the returns. For example, instead of paying 1% for every €1 below €75 in the initial example above, a government could promise to pay 10%. A real sign of commitment to preventing climate change. Leverage would also become available as investment banks are likely to take index-linked carbon OATs and ‘strip’ them into their component parts, reselling it as a pure option on government commitment and a zero-coupon government bond.

Governments claim they are serious about meeting carbon emission targets, serious about moving to a low carbon economy. Governments are likely to issue a large number of OATs over the next few years due to the credit crunch, and the need to balance external deficits with debt . By issuing carbon bonds linked to independent, auditable index metrics such as emission targets, the price of fossil fuel and the future carbon price, governments would remove private investors’ objections that their biggest uncertainty is government commitment. Likewise, given that failure to perform will cost, government would have a real incentive to meet its emission targets. Finally, government debt itself is likely to become a highly competitive market, and index-linked carbon OATs might well be a way of differentiating government debt to make it more attractive.

The problem is not investment; it’s confidence. Unlike other ideas, though not to exclude them, government PPBs require no central planning or management, any credit-worthy government can issue them. The funds raised need not be hypothecated, but government carbon policy performance bond prices would provide a real indicator of confidence in government actions. Government carbon policy performance bonds would remove the biggest risk stymying low carbon project developers, lack of confidence in governments enforcing their own policies.

Example 2 – Corporate NOx Policy Performance Bonds

In September 2015, environmental regulators found that German automaker Volkswagen Group had intentionally programmed turbocharged direct injection diesel engines to activate certain emission controls only during laboratory testing. The software allowed the vehicles' nitrogen oxide (NOx) output to meet regulatory standards during testing but produce up to 40 times higher NOx output in real-world driving. At the moment, Volkswagen appears to have applied this ‘cheat’ to an estimated eleven million cars worldwide. In October 2015, the Volkswagen crisis deepened with ‘irregularities’ surrounding the fuel consumption measurements and carbon dioxide (CO2) emitted by 800,000 cars.

The scale of the deceptions, number of recalled automobiles, environmental damages, effects on health, and even the death toll largely due to heart and lung disease, are still unclear. The UK’s Department for Environment Food & Rural Affairs believes “that the effects of NO2 on mortality are equivalent to 23,500 deaths annually in the UK.” [1] Transport is about 47% of UK NOx emissions, but “around 80% of NOx emissions in areas where the UK is exceeding NO2 limits are due to transport”. The European Environment Agency estimates NOx emissions due to transport at around 46% across Europe. [2] Researchers wonder “if strategies used by manufacturers to fool the testing system have contributed to the unexpected failure of countries to reach NOx targets.” [3] While the extent of the swindle is still being calculated, the ramifications of the scandal in distrust of automotive manufacturers, regulators, politicians and business are even murkier. So could a novel, yet simple, approach ensure that future regulatory structures provide a school of hard financial knocks to automotive firms that transgress policy objectives: environmental policy performance bonds.

Automotive firms, like Volkswagen, could be forced to sell appropriate environmental ‘policy performance bonds’ in order to enter national markets. One form of policy performance bonds might be NOx bonds’. NOx bonds would link bond interest payments to a NOx emission reduction target. An investor in a NOx bond receives an excess return if the issuing firm’s environmental reduction targets are not met. For example, the bond might pay an extra percentage point of interest for each 5% an automotive company’s emissions are above a target.

Failure to meet targets means higher interest payments to investors. NOx targets could be linked to the number of car sold in a specific region (Europe or the USA for example) or country. If the company or companies achieve NOx reduction objectives, no extra interest is paid. If it fails, it could pay a punitive interest rate depending deviation from the target. The bonds would align financial and environmental incentives and help automotive firms regain customer and investor confidence.

A government would set out appropriate environmental targets, e.g. average NOx levels from sampling stations a decade ahead, or overall CO2 emissions by vehicles, or average end-user fuel consumption per automotive kilometre travelled. These targets would be linked to a variable bond interest rate, e.g. a base rate plus 1% interest per percentage point a target is exceeded. The effect of a 10% overshoot of NOx targets on a bond with a base rate of 5% would be a bond that paid 15%, quite a significant interest rate. Automotive companies would be uncomfortable issuing such bonds unless they were clear that they intended to ensure targets were met.

An acceptable base rate is likely to be set by the market at slightly less than a traditional automotive bond, largely because there is some significant upside for an investor if firms in aggregate fail to achieve the target. Firms issuing such bonds ought to hope for low base rates while there is uncertainty. In effect, investors should be providing firms with loans at below typical base rates in return for betting against them on achieving targets. The maturity date for the bonds should be set over a reasonable time period, perhaps a decade.

Of course, the net effect is to encourage appropriate investment in achieving pollution reduction targets. If the low-pollution future fails to arrive, automotive firms wind up paying investors higher interest rates on their debt. If the low-pollution future does arrive, automotive firms had the incentive to help deliver it. If firms tell the truth, they get cheap money. If firms are not committed, they pay.

There are some obvious niggles. Not all transport companies are equal. Firms might be ‘encouraged’ to issue bonds in line with sales or market share or calculated pollution. Not all NOx or CO2 or fuel consumption is transport. This observation leads to considering widening the scheme to other sectors. Equally, it invokes caution in ensuring the bonds are effective sticks but not punitive instruments. Further, these could be group targets, e.g. automotive emissions in total for a country. As a group target, automotive bonds might encourage a more systemic approach working together on traffic reduction or advanced technologes. As a group target, firms would have an incentive for policing each others’ compliance. In an ideal world, the automotive industry might issue a ‘funding principles aligning financial and environmental incentives’ report each year.

With so much uncertainty about automotive company morals, firms will need ways to distinguish themselves in a crowded market. They also urgently need to regain stakeholder’s confidence and to act instead of react, waiting for financial punishment from regulators. The more firms issued such bonds, the more convinced the market would be that they indeed intend to contribute to reducing emissions and achieving other environmental targets.