Edgy – Central Bank Digital Currencies Could Cut A Number Of Ways

Wednesday, 10 February 2021By Professor Michael Mainelli

[An edited version of this article first appeared as "Edgy – Central Bank Digital Currencies Could Cut A Number Of Ways”, Michael Mainelli, Digital Bytes, TeamBlockchain (10 February 2021), pages 8-11 - Chinese translation. You can also listen to Digital Bytes Blockchain Radio programme on same.]

The Next Evolutionary Stage Of Money, CBDC?

Numismatists in the United States refer to reeded edge coins as ridged, with the US quarter having 119 ridges, while people in the United Kingdom refer to them as milled. Central Bank Digital Currency (CBDC) experiments are becoming increasingly ‘edgy’ as various pilots around the world by central banks begin to provide outlines of where CBDCs might go. And this edginess could cut in a number of ways.

First, a few definitions. Money is a technology community use to trade debts across space and time. Fiat money is government-issued currency that is not backed by a physical commodity, such as gold or silver, but rather by the government that issued it. Fiat currency’s value is derived from its monopoly on paying tax, in effect the national community trades tax debts. Fiat currency is ‘backed’ by the government’s extensive enforcement of taxation.

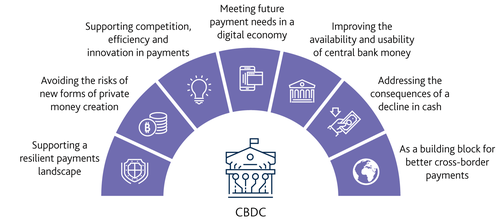

CBDC refers to a variety of proposals involving digital currency issued by a central bank, effectively moves towards a wholly digital fiat currency. The latest Bank for International Settlements (BIS) survey on CBDCs summarised the current situation: “Most central banks are exploring central bank digital currencies (CBDCs), and their work continues apace amid the Covid-19 pandemic. … A testament to these motives is the launch of a first “live” CBDC in the Bahamas. This front-runner is likely to be joined by others: central banks collectively representing a fifth of the world’s population are likely to issue a general purpose CBDC in the next three years. However, the majority of central banks remains unlikely to issue CBDC in the foreseeable future.” The purported benefits of CBDCs were set out clearly by the Bank of England in a March 2020 report, from which the following diagram is reproduced:

CBDC Is Emphatically Not Distributed Ledger Technology

Yet the history of technology deployment, from gunpowder to vaccination to atomic power, always seems have two edges, good and bad. Moving the entire ‘operating system’ of the economy onto new technology is a big decision, and I welcome the caution and experimentation central banks are putting into this thinking. Clearly, the first big risk is having a potential ‘single point of failure’.

Cryptocurrency and blockchain proponents often claim that central banks will use cryptocurrency or distributed ledger or smart ledger technologies to provide e-money. While portions of such technology may be used, e.g., using smart ledgers as independent authoritative timestamping engines for backup, CBDCs are emphatically not cryptocurrencies and have no particular need to use distributed ledger technologies. As Sweden’s Riksbank concluded: “From a purely technical point of view, we can see nothing at this point in time that would prevent an e-krona solution built around a central register. RIX, the Riksbank’s system for the transfer of funds in accounts, is, for example, built around a central register. An e-krona could in principle be constructed in a similar way.” Blockchain and distributed ledger technologies have about as much relevance to CBDCs as databases, networks, smartphones, and other obvious underpinnings to digital applications. Distributed ledger may be used but isn’t essential.

What We Have Here Is A Failure To Communicate Fractional Reserve Banking

In July 2016, giving evidence to the House of Lords Economic Affairs Committee [Blockchain Technology Explored By Economic Affairs House of Lords Committee: Watch 15:50 To 16:32], I speculated on a few things about CBDCs that are becoming increasingly prominent, principally the role of CBDCs in money supply and taxation, as well as a deeper point about fractional reserve banking. Do bankers understand the deep political and social implications of what looks like a technical and economic project?

Discussions about inequality continue to rise in volume and importance. CBDCs will raise intense, even unpleasant discussions about the nature of money and leverage. Antonio Banderas’s character in a film about the Panama Papers, The Laundromat, says “Credit is just the future tense of the language of money.” CBDCs could cut to the core of banking credit soon. Private sector bankers use your deposits to leverage their lending, i.e., fractional reserve banking. When the Bank of England comes and shows you a CBDC that they want you to use, and prove it’s secure, why would you want to deposit it anywhere other than the Bank of England? Why do you need a private sector banker?

Private sector bankers need to prove that they are interested in building a better society as a first step towards restoring credibility in financial services. Personally, I would suggest a project to create a manifesto for ‘Credit Creation In The Modern Economy: A Discussion Of Leverage, Economy, And Society’. Fractional reserve banking may be at risk as never before. Interestingly, this year the Swedish banking sector belatedly appeared to appreciate this risk as discussions of their future role in a CBDC system nettled them.

Quantity Has A Quality All Of Its Own

The quantity theory of Money, MV = PQ, i.e., the total amount of money (M) times the velocity of money (V) equals the average price level (P) times the level of output (Q), has a shaky empirical basis. All that central bank navel-gazing and monetary prognostication has often been so much augury and astrology. This is not surprising as quantity and velocity have never been known with any accuracy, and so the models remain largely unproven. CBDCs will provide M and V to a high degree of accuracy. Further, they can also provide missing variables, my suggestion being to include distribution and biodiversity measures in monetary system evaluation. This could be a radical improvement in monetary systems management, though a further discomfort to the private credit creation in fractional reserve banking.

Facebook Quality Privacy From Your Central Bank

CBDCs raise a unique opportunity to fight crime. Unlike contemporary fiat currency, each individual tax credit can be tracked. It’s as if the serial numbers that already exist on paper money were being recorded in transactions so you could examine the entire history of the banknote you received in exchange for a newspaper a second ago back to its issuance by the mint. Despite the reassurances we will receive, the power is there, and it is hard to put such technological genies back in their bottles. If you don’t have something to hide, why would you object to a CBDC tracking all your purchases and personal transactions? Obviously, the government is trying to clamp down on criminals, tax evaders, and money launderers. It’s just a shame that whatever hobby you’ve been spending on suddenly becomes socially unacceptable and lists of those spending on it are now public shame lists.

Godwin’s Law Of Economics? Taxation Nazis

American attorney Mike Godwin's law of Nazi analogies is an internet adage that “as an online discussion grows longer, the probability of a comparison involving Nazis or Hitler approaches 1”. I might coin a parallel law of economic discussions, “as an economic discussion grows longer, the probability of creating a new form of taxation approaches 1”.

CBDCs provide the power to apply complex algorithms to taxation on any transaction in real time. Once people realise the power of CBDC systems to support various taxation initiatives at low transaction costs, expect thousands of proposals, local town taxes, child taxes, sugar taxes, alcohol consumption taxes, or foreign visitor expenditure taxes. I once gave an example of a tax, only possible because of CBDCs, a geographic redistribution tax whereby the tax on transactions rose in wealthy districts. For those outside London interested in levelling up the taxation rate increases as you approach Trafalgar Square whereupon it reaches 99.9%. Spend your money in the Outer Hebrides.

No Small Change

British economist William Stanley Jevons (1835–1882) coined a couplet, "Money is a matter of functions four: a medium, a measure, a standard, a store." It seems desirable that money should be a stable medium, measure, standard, and store. But money seems to evolve in leaps of ‘punctuated equilibria’ speeding up as they move along, through Sumerian clay tablets, Egyptian papyri, Lydian gold, Chinese paper, medieval tally sticks, metal currencies, gold standards, central banks, and digital services. It’s likely to evolve again soon. We need to pay more attention to the edgy political and social implications of the next likely punctuated equilibrium and the upheaval they may cause. CBDC may well stand for Central Bank Dynamic Currencies.