Disrupting Dividends – The Case For Revenue Share Tokens (RSTs)

Thursday, 14 May 2020By Chris Wickham

Revenue Share Tokens (RSTs) could well provide the optimal funding solution for early stage businesses. Currently, financing options for young companies in both Western Europe and North America are not only limited but could also create economic shortfalls at a time when “new economy” firms seem likely to generate the bulk of mature market GDP growth. Given traditional funding sources appear virtually dead, a solution is needed. In this short paper, put together by www.blockchainanalytica.io the advantages of RSTs over current sources of finance are explored.

Business expansion finance for early stage companies is probably on the verge of its most radical shake-up for some time. Put simply, the traditional potential sources of finance do not satisfy younger companies’ needs. Commercial banks, investment banks, private equity and venture capital, with due regard for favourable tax treatment, have generally failed in their potential reliably to finance to early stage growth companies.

Revenue share tokens (RSTs) are relatively simple and cost effective to mine, mint and create. Each issuing company creates a blockchain with integral smart contracts, which deliver an income stream to the token holders, based on the revenue of the company. It should be noted that reported revenues are prone to far less subjectivity than reported profits.

The way that RSTs work is simple. The holder of a token receives a given share of a company’s revenue in return for having invested in that token. The issuing company is obliged to allocate a pre-determined portion of its revenue to its RST token holders. These distributions are a cost to the company which is struck between the gross profit and EBITDA lines of its accounts. As revenue rises so do the RST pay-outs.

Cryptocurrencies issued by companies in the form of a pure Initial Coin Offering proved to be a short-lived attempt to disrupt incumbent, albeit inadequate, sources of finance. The lack of any clear association between an issuing company’s performance and the value of that company’s tokens proved pretty much universally fatal. Ironically, the dominantly traded cryptocurrency remains Bitcoin, which has never acted as a source of corporate finance.

But crypto currencies, in the form of revenue share tokens, have the potential to generate substantial change. In our view, they should be the “go to” source of funding for any company looking to raise early stage expansion capital. In particular, they provide a clear relationship between a company’s commercial success and the value of its token. Moreover, they return an estimable pre-defined income stream to token holders while allowing the issuers total control of their businesses and avoidance of any dilution. Put simply, disruption of the dividend model is a “win:win” for both sides.

Valuation of a revenue share token is very straightforward. It is the present value of future pay-outs depending on assumptions of revenue growth. There is no opportunity, in contrast to equities, for profit and dividend pay-out based valuation models to bifurcate due to management strategy, leverage and free cash flow issues. Revenue is is very definable and the token holders earn a fixed share of it each year.

Overview

This report makes the case for the issuance of and investment in revenue tokens. The focus is on early stage companies which require expansion capital. However, the issue of such tokens could well suit larger organizations which still require capital to grow. Overall, the conclusion is that revenue tokens should be one of early stage companies’ considered routes to expansion capital. These tokens enjoy clear advantages relative both to private equity and various forms of debt instruments.

Furthermore, a strong source of funding for expansion finance should receive significant government and associated regulatory support. In particular, the combined HM Treasury, Financial Conduct Authority and Bank of England 2018 publication Cryptoassets Taksforce: final report made two opening assertions. First, the authors stressed the importance of the City of London being a dynamic financial centre. Second, it prioritised funding for early stage companies. Far from being a villain, cryptocurrencies are seen as a potential economic solution for early stage companies’ financial needs. As the report stated:

“The government has set out an ambition for the UK to be the world’s most innovative economy and to maintain its position as one of the leading financial centres globally.” And;

“The Taskforce has concluded that if benefits develop in the future, they are most likely to materialise through the use of ICOs as a capital raising tool. ICOS have the potential to present a range of opportunities.”

But cryptocurrencies and digital assets (d@ssets) alone will not satisfy investors’, fundraisers’ needs and regulators’ desires. What is important is that tokens which have the potential to be taken seriously by investors incorporate both fiduciary and financial attractions. Fiduciary can be supplied by blockchain. Financially what matters is the income stream associated with revenue sharing.

Revenue Tokens – Disruption in More Detail

The Basics

A revenue token is effectively a security issued by a company in return for a pre-agreed sum of money, which entitles the purchaser to a share of the issuing company’s future revenue. As the company’s revenue expands so too will the amount paid out in the form of revenue share. Similarly, the value of the token should increase as it yields more. Put simply, the token is a play, arguably an option, on the future revenue growth of the issuing business.

Revenue share tokens are issued by companies which look to raise capital by securing the funds raised for the investors against future revenues. The tokens are issued in the normal way through an intermediary.

A revenue share token will most likely comprise a blockchain enabled smart contract where the company’s revenue is immutably registered on the blockchain. A predetermined portion of that revenue will be returned to the token holder. For example, if a company issues a 7% RST the tokenholders will be entitled to 7% of that company’s revenue in any given year.

For accounting purposes the revenue share would be treated as an operating cost, equivalent to any other payment made in the normal course of business but not associated with costs of goods sold. RST pay-outs should be seen as a cost similar to items such as advertising & marketing, rentals and wages. While they assist financing, they are not a finance cost for accounting purposes. The pay-outs sit firmly between the gross profit line and EBITDA.

Disrupting Bank Finance

Being blunt, there is comparatively little bank finance to disrupt. As we illustrated earlier, UK bank loans outstanding to small and medium sized enterprises are a tiny fraction of those allocated to mortgages. Moreover, early stage businesses find it nearly impossible to raise finance through bank loans. As discussed, these companies have minimal collateral to offer.

Disrupting Dividends

Disrupting dividends is effectively the process of disrupting equity finance. The value of any equity investment is the present value of its future dividend stream. This holds true in the case of both investments held for their organic potential and exits. Without the expectation of a dividend return at some stage, an equity is valueless. Importantly, dividends may only be paid out to shareholders from accumulated profits. In the event of a company not being profitable, it is not able to reward investors with an income stream.

But revenue share tokens reward investors instantly. The payments to those who financed the business are mandated by the smart contract, which is itself immutably recorded on the blockchain. There is no potential for investors’ revenue share payments to be reduced or cancelled on the basis of management policy or grounds of UK company law.

Valuing Revenue Share Tokens

Valuation of revenue share tokens should be reasonably straightforward. The tokens’ present value is a basic discounted cash flow calculation where future cash flows are represented by the actual revenue shares. In addition, a yield can be applied as a cross check.

Moreover, valuation of an RST should reflect the transparency of any pay-out. Once the company’s sales revenue has been forecast – typically the most visible income statement item – the RST pay-out becomes a residual. It is an immutable function of the company’s top line.

Revenue Share Tokens in Practice

Revenue share tokens are relatively simple to illustrate. Indeed, their simplicity is a significant attraction to the investor given that the pay-out is directly related to the company’s revenue. Moreover, the definitions of revenue and resultant size are built immutably into the smart contracts which are in turn embedded into the blockchain. The attractions to investors should be as clear as the instruments themselves.

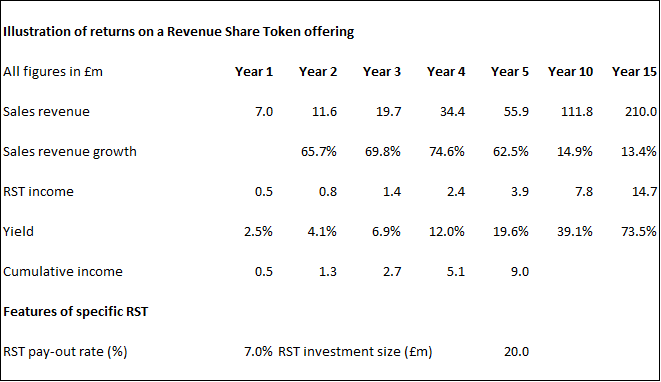

In Figure 1, we use the example of a fast growth company which issues a 7% RST – i.e. the company is mandated to pay-out 7% of its revenue annually to the token holder. As can be seen from the example, the token holders recoup entire value of their initial investment relatively quickly through dividends – almost half is returned by the end of Year 5.

Moreover, they enjoy some very attractive yields on their investment at an early stage of the process. In this example the Year 3 yield is an impressive 6.9% and continues to increase thereafter. So long as the company’s revenue continues to increase so do the token holders’ returns.

Figure 1 – Revenue Share Tokens In Practice – Illustrated Example

Source: Blockchain Analytica estimates

Current Financing Options – The Case for Change

Bank loans

Bank debt, even when desired by early stage companies, is conspicuous by its lack of availability. Put simply, large commercial banks are B2C businesses and not corporate financiers. Our own repeated observation for early stage companies which look to raise funds beneath around £5m is that corporate bank debt is rarely an option.

For even smaller “friends & family” size raises the more likely debt option for an entrepreneur would be a house re-financing via an incremental mortgage than any entry level entrepreneur’s loan. In general, banks do not lend where there is minimal collateral. Moreover, early stage companies’ default risk profiles are typically too high to be associated with unsecured debt.

Bank of England data for bank loans outstanding at end-August 2019 are shown in Figure 2. What is interesting is the extent to which mortgage lending eclipses lending either to large businesses or small businesses. Mortgages outstanding at end-August 2019 were valued at £1,431.4 billion. Outstanding loans to large corporates on that date was £318.9bn while consumer credit outstanding was £218.6bn.

Loans outstanding to small and medium enterprises were lower still at £167.0bn. However, if property related loans to SMEs were excluded the number would be even lower still at £99.4bn – i.e. mortgages are effectively 14.4x more important to the UK commercial banking sector than early stage finance. Unless they re-mortgage their residences, entrepreneurs need to look somewhere else than to UK banks for funding.

Figure 2 – UK Bank Lending by Key Category – Loans Outstanding in £bn

Source: Bank of England Data

Loan notes

Loan notes drafted by non-bank financial institutions and similar corporate bonds tend to be exceptions rather than the rule for early stage companies. Rather, they tend to be tools used by established firms.

A disadvantage for very early stage businesses is the cost of servicing the debt. Moreover, they can be expensive to arrange – typically of the order of 5.0% of funds raised – and create a charge over the borrowing company. Such charges in difficult circumstances can lead to foreclosure and enforced bankruptcy of early stage businesses, which is by no means ideal.

Equity Finance – Private Equity and Venture Capital

Small scale equity finance is a credible option for smaller, young companies. However, there are disadvantages for both sides. While the fundraising business avoids interest costs, the entrepreneurs – i.e. founding shareholders – themselves suffer the disadvantage of dilution.

Moreover, the investors tend to be minority shareholders in the concerns with little recourse to dividends or influence on strategic thinking. Should they become larger shareholders with more managerial sway the problem decreases. However, that is often to the detriment of the entrepreneur.

The primary benefit of PE and VC funds is tax. But while the investors enjoy the tax benefits of their activities, they often do not have the administrative time or risk appetite to invest in very early stage businesses. Risk profiles are frequently too high and investable amounts too low to make commercial sense. In addition, such tax benefits accrue only to the investor.

Equity Finance – Crowdfunding

Established crowdfunding platforms clearly do a good job. The commitment of such organizations to early stage businesses’ growth is obvious, not least because they tend to become investors in the companies which they fund. There are a number of pros to crowdfunding.

However, there are cons. First, the process can be expensive. Charges tend to be of the order of 7% with the raising company taking an equity stake in the form of carry. Second, the process is very public. In order to encourage largely private shareholders to purchase stakes in businesses, a fair amount of disclosure has to be given. Third, there is the risk of deals not meeting their minimum raise required – i.e. the soft cap – before funds can be used.

Furthermore, there is an argument that crowdfunding appeals to a relatively narrow investor cohort. Private individuals make the investment decisions and probably lean towards familiar territories – consumer goods, retail, traditional industrial and commercial activities. As much of the activity we envisage for early stage entrepreneurs involves newer industries – AI, applications, blockchain, fintech, machine learning, technology etc. – crowdfunding is arguably not their natural home.

Cryptoassets – Moving Swiftly Forward

Pure Cryptocurrencies

Pure cryptocurrencies which do not act as a platform for other currencies in the way that Ethereum does, should have limited appeal for early stage companies and entrepreneurs in our view. The most obvious and dominant of these – Bitcoin – exists largely as a store of value. It benefits from being both non-domiciled and readily tradable into fiat currencies.

But while it has never claimed to be a source of industrial and commercial finance, Bitcoin laid the foundations for other tokens and proved the concept of blockchain based currencies and tokens with an integral use of smart contracts.

Tokenisation – the early years

Initial Coin Offerings, Securitised Token Offerings and Initial Exchange Offerings were the early, acronym inspiring, methods for businesses to raise funds. All three proved problematic so far partly because the closer they resembled traditional securities the more challenging became the regulation.

ICOs were very fashionable in 2017. However, they encountered criticism for giving companies an effective carte blanche regarding how funds might be used and offered little in the way of any return to investors – guaranteed or not. Indeed, their fashionable period ended so abruptly and arguably catastrophically that it became referred to as the “Wild West era.”

Security Tokens are arguably equities marketed in encrypted format. Their advantage is simplicity of manufacture (effectively minting or mining) and ease of valuation. They proxy equities and therefore can be valued based on long-standing formulae. However, they have received stark resistance from regulators – notably in the US.

IEOs effectively use exchanges to raise money for the entrepreneurs in contrast to investment banks, stockbrokers and other fundraising platforms. However, the benefits to the investor of pure cryptocurrencies over and above Bitcoin have proved questionable.

Similar to the way in which gold is the only element which proxies a currency, Bitcoin is the only cryptocurrency truly to proxy money at this stage. As a result, cryptoassets will have to offer something materially positive to investors if they are to grow in importance as a fundraising source for early stage companies.

Conclusion

Revenue share tokens are well placed to be at the forefront of capital raising activity associated with blockchain and cryptocurrency. They demonstrate a clear capability of satisfying both issuing companies’ and investors’ needs simultaneously while being capable of delivering superior investment performance to both debt instruments and equity.