When The Safe Asset Needs Saving - Is The US Treasury Market Still Safe Enough To Be Saved?

Monday, 29 June 2026By Yuan Gao

Every financial system keeps one asset it treats as gravity — the fixed-point other prices fall towards; the place crises are meant to go to die. For the dollar world that asset is the US Treasury: the collateral base of the repo system, the benchmark against which every dollar asset is priced, and the instrument reserve managers hold when they want liquidity rather than adventure. Treasuries are not simply another market. They are the anchor.

So, it should unsettle us that, twice in six years, central banks have had to buy the safe asset to keep it safe.

The Rescuer That Needed Rescuing

In March 2020, during the dash for cash, the world’s deepest market stopped functioning, and the Federal Reserve bought roughly a trillion dollars of Treasuries in three weeks to restore order. In October 2022, the Bank of England intervened in the gilt market after liability-driven pension strategies turned falling prices into forced selling. Different countries, different investors, different instruments — the same mechanics.

Those mechanics are easy to state and hard to stop. Leveraged or constrained holders are forced to sell; their selling moves prices against them; the move triggers the next margin call, redemption, or collateral revaluation, which forces still more selling. A shock becomes a loop. Reflexivity is not just a theory of market psychology; in the safe-asset market, it becomes plumbing.

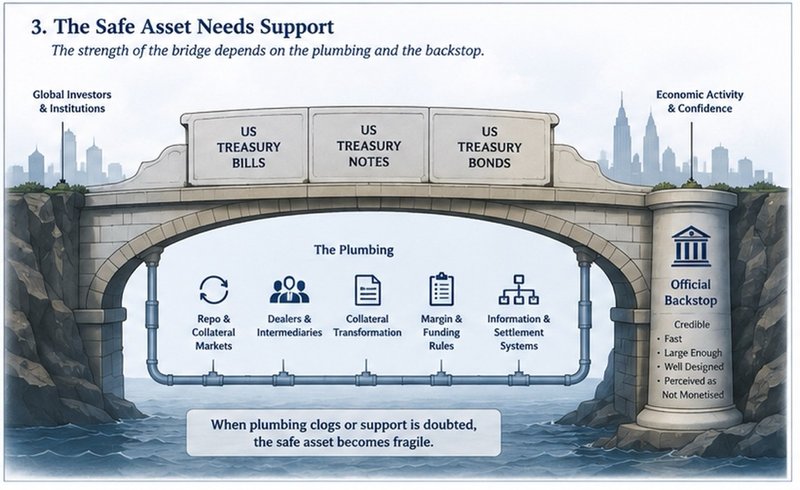

Safety Is A Property Of The Network, Not The Issuer

We usually argue about sovereign safety as though it were a property of the borrower: deficits, debt-to-GDP, credit ratings. But March 2020 and October 2022 were not solvency events — no one doubted that the United States or the United Kingdom would pay. The markets broke at the level of structure: the holders, dealers, repo lenders, hedge-fund basis trades, collateral rules, liquidity buffers and, increasingly, digital redemption channels that sit around the asset.

A safe asset, in other words, is safe only if the network around it can absorb selling without converting it into more selling. That turns Long Finance’s animating question — when would we know our financial system is working? — into something sharper and testable: when would we know the safe asset is safe?

What Seven Doom-Loops Teach

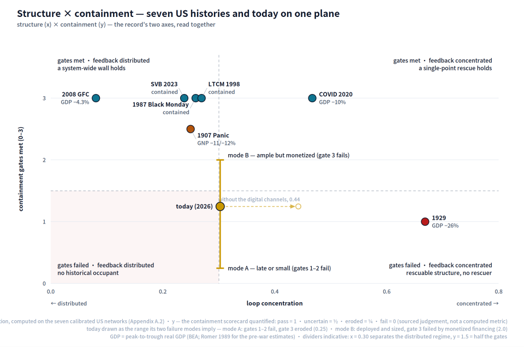

History disciplines the question. In recent work I rebuild seven US “doom-loops” as networks — the Panic of 1907, the 1929 margin collapse, the 1987 portfolio-insurance crash, the near-failure of Long-Term Capital Management in 1998, the 2008 crisis, the March 2020 Treasury seizure, and the 2023 Silicon Valley Bank run. They differ in instruments and era but share a family resemblance: a leveraged or confidence-sensitive balance sheet, a funding or collateral clock, and a price or solvency move that forces the next round of selling.

The uncomfortable lesson — for modellers and policymakers alike — is that structure identifies fragility but does not decide the outcome. The 1929 system was structurally simpler than most modern crises, yet it produced the deepest collapse, because no effective lender of last resort came. The 2008 system was more deeply coupled and more dangerous, yet it was contained, because the rescue was broad, fast and credible. Structure sets the fragility; the backstop decides the fate.

Why Today Is Unusual On Both Counts

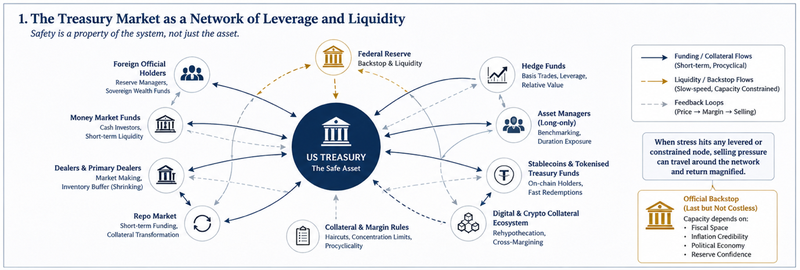

That distinction matters because today’s Treasury market looks stretched on both axes at once — which, a configuration I do not find in the seven reconstructed US cases.

On structure, the market is far larger, dealer balance-sheet depth is thinner, and the marginal buyer is now a leveraged one. The cash-futures basis trade has made a handful of hedge funds a central transmission channel; repo is the plumbing through which stress travels in hours; and newer channels — stablecoins, tokenised Treasury funds, crypto collateral — open redemption and liquidation routes faster than the 2020 playbook assumed.

On the backstop, the United States still holds the “exorbitant privilege” of issuing the world’s reserve asset. But privilege is a convention, not a law of nature — a confidence structure that can erode. Public debt is higher than in past rescues, interest expense is heavier, inflation credibility binds harder, and reserve managers, meanwhile, have been adding gold at the margin, a quiet signal that the safe-asset hierarchy is no longer entirely automatic. The Federal Reserve can still support market functioning. The harder question is whether such support would be read as costless liquidity provision — or as fiscal accommodation through the central bank’s balance sheet.

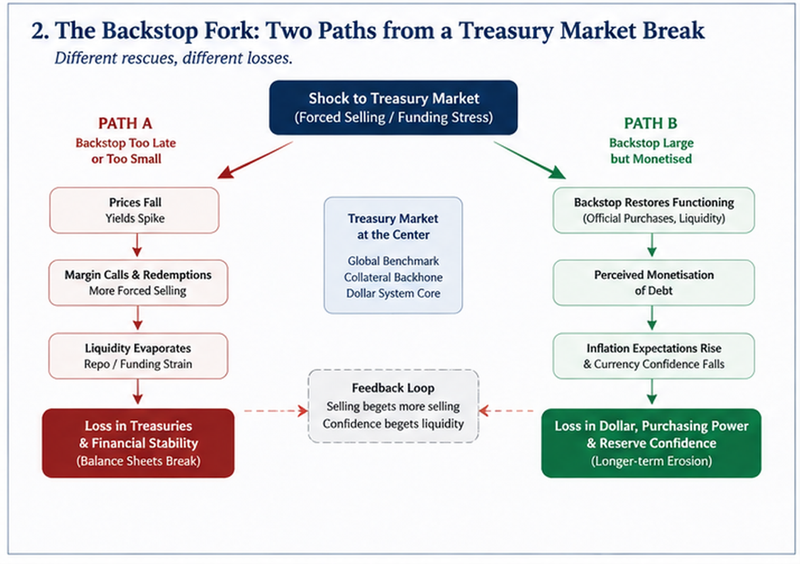

The Fork

So the honest forward statement is a fork, not a forecast. If a break comes and the backstop arrives too late or too small, the loss shows up where we expect it — Treasury prices, repo, leveraged balance sheets — the familiar forced-selling failure. But if the backstop arrives large and fast yet is perceived as monetised, the loss migrates: into the currency, inflation expectations and gold. In the first path the safe asset fails because it is not rescued; in the second, it is rescued in a way that makes the rescue itself the next loop. Which tail materialises is decided not by structure but by the backstop’s credibility.

Structure × containment: seven US crises and today on one plane. The horizontal axis measures how concentrated the feedback is; the vertical axis, how many containment gates a rescue met. Today enters not as a point but as a fork. Source: Gao 2026, “The Geometry of Market Fragility.”

From Forecasting To Measurement

None of this predicts an imminent crash — and that is the point. Forecasting the next price move is the wrong defence: under stress, prices are set by the interacting forced decisions of the very holders under examination. What can be measured in advance, from public data, is the structure — where the leverage sits, which loops carry the break, where pressure can drain, and whether the public backstop is still fast, matched and affordable.

That is a long-finance posture rather than a trading call. It argues for treating the safe asset’s safety the way we treat a bridge’s load rating: something measured continuously and in the open, not assumed until it fails. The raw materials already sit in public data — basis-trade positioning, dealer utilisation, repo, the dollar–yield correlation, the gold share of reserves. A standing, reproducible “fragility gauge,” updated and public, would let officials pre-position rather than improvise — an evolution, not a revolution, in how we watch the anchor of the system.

So the practical conclusion is a posture, not a date. Watch the basis trade. Watch dealer capacity. Watch repo. Watch whether dollar weakness begins to coincide with rising Treasury yields. Watch whether gold keeps gaining at the margin. Above all, watch whether the market still believes that the institution standing behind the safe asset is itself safe enough.

The safe asset may well still be safe. But in a more leveraged, faster and more politically constrained financial system, its safety is no longer something to assume. It is something to measure.