Financial Services & Climate Change: More Than Hot Air?

Monday, 03 December 2018By Simon Mills

This article is an extract from the second edition of the Global Green Finance Index (GGFI), which was published in September 2018. The GGFI is compiled from a global survey of financial professionals, combined with quantitative data extracted from 113 independent sources.

The Challenge

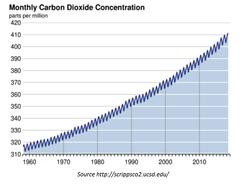

Atmospheric concentrations of greenhouse gases have risen precipitously since the beginning of the Industrial Revolution. For carbon dioxide, the average concentration has increased from 282 parts per million (ppm) in 1800 to 412ppm in 2017.

The last time CO2 levels were this high was the middle Pliocene, 3.6 million years ago. During this period, global temperatures were 2° to 3° C higher than today[1]. Forests grew across the Arctic[2] and global sea levels were 25 metres higher than today[3].

Inertia built into climatic systems means there is a lag between rising CO2 concentrations and the impact on global temperatures. The full impact of carbon emissions today will not be felt for half a century[4]. However, if all known reserves of fossil fuels were burnt, average global temperatures would rise by 10o C[5], rendering 99% of life on earth extinct.

To survive, society not only has to transition economic growth onto a low carbon path that keeps temperature increases below 2o C; it must also adapt infrastructure and services to cope with the impacts of climate change.

The Role of Financial Services

The financial sector is a critical means for price signals, regulation, and civil society pressure to create and direct financial capital to more or less sustainable economic activity. International and regional financial institutions, finance ministries and central banks all have crucial parts to play in achieving the goals set out in the Paris agreement and the Sustainable Development Goals[6].Financial services affect development paths in three main ways:

- Pricing assets and exercising ownership;

- Pricing Risk; and

- Flows of finance.

Policy makers, finance ministries, regulatory agencies and central banks have an enabling role in ensuring adequate transparency and governance, providing a level playing field and ensuring a stable policy environment in which long-term investment can take place.

Are Financial Services Living Up To The Challenge?

Pricing Assets and Exercising Ownership- It is estimated that world-wide, 20 per cent of all funds are now managed on Socially Responsible Investment (SRI) principles[7]. Globally there are now $22.89 trillion of assets being professionally managed under responsible investment strategies, an increase of 25 per cent since 2014[8]. Impact investment funds grew from $25.4 billion to $35.5 billion between 2013 and 2015.Pressure is ramping up on businesses. The Carbon Disclosure Project now collects information on climate risks and low carbon opportunities from the world’s largest companies on behalf of over 650 institutional investor signatories with a combined US$87 trillion in assets.Shareholder activism is also increasing with pressure being placed on fossil fuel companies for disclosure of risks associated with ‘stranded assets’[9].

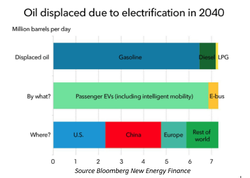

Pricing Risk- Climate concerns and technological changes are creating new pricing risks, dramatically illustrated by the collapse in value and bankruptcies of several US coal companies in recent years[10]. The rise of electric vehicles[11], overcapacity, stranded assets, and pricing issues are still major risks for fossil fuel and related industries[12].

It is thus no surprise that Stock Exchanges around the world are embracing market transparency on climate and other impacts – 23 stock exchanges currently incorporate reporting on environmental, social and governance (ESG) information into their listing rules and 15 provide formal guidance to issuers[13].

ESG analytics has long been a key tool for specialist SRI funds. Increasingly, it is being used in relation to mainstream investment analysis and is becoming a factor used by rating agencies[14].

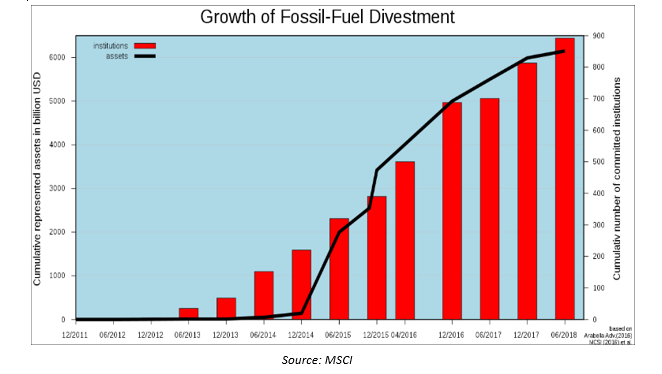

Momentum is growing on disinvestment and structured disinvestment with a number of high profile sovereign funds, including Ireland and Norway, reducing or completely cutting their holdings in fossil fuel companies.

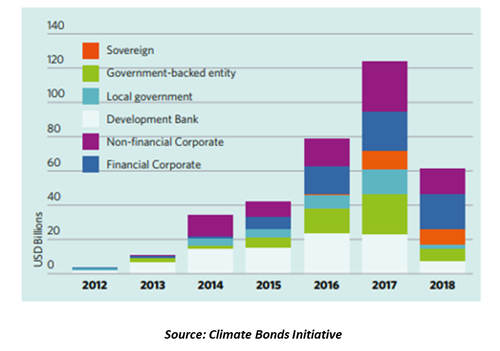

Flows of Finance- The Global growth of green bond markets has played a significant role in raising the profile of green finance. Globally, 14 stock exchanges now have dedicated segments for green or sustainable bonds[15], and there has been strong growth in the issuance of green bonds - with 2016 seeing the issuance of the first sovereign green bonds.

Financial Centre Leadership

Whilst national policy-makers seek to capitalise on what is perceived as a new market opportunity, through a variety of national programmes, for financial centres the emphasis is very much a focus on collaboration, cooperation and the sharing of best practice. Initiatives such as Financial Centres for Sustainability[16], the Sustainable Stock Exchanges Initiative[17], and UNEP FI[18] continue to provide valuable resources which are encouraging the growth of the green finance sector.

A Mountain Yet To Climb

The transition to a green economy, required if the world is to meet the targets laid down in the Paris Agreement and avoid catastrophic climate change, is a huge global investment opportunity: the International Energy Agency (IEA) estimates that $26 trillion of additional investment is needed just in renewables and energy efficiency between 2015 and 2040 to achieve the 2°C target – around $1 trillion a year – not including the large amounts also needed for climate mitigation[19].However, green finance has a long way to go if it is to penetrate and displace the enormous amounts of finance for carbon intensive activities, or “brown finance”. In 2016, global climate finance flows were $383 billion, less than half the $ 1 trillion a year needed under the IEA estimate[20]. Only five to ten percent of bank loans are “green”[21] (based on data from the few countries where national definitions of green loans are available), and “brown” finance flows still massively overshadow green finance even in the public sector: G20 countries alone received USD 72 billion in annual public financing for fossil fuel energy production between 2013 and 2015, and only $18.7 billion for clean energy [22].In 1960, the carbon intensity of the world’s GDP was 1,000 gr CO2 per $. By 2000 this had dropped to 500 gr CO2 per $. In 2010 this had reduced to 400 gr CO2 per $. Despite this rapid progress, if we are to have any hope of attaining the Paris target of limiting global warming to 1.50C the carbon intensity of GDP must be below 60 gr CO2 per $ by 2050.The progress made by the centres listed in the Global Green Finance Index is heartening, but there is a mountain yet to climb.

References

[1] Robinson, M.; Dowsett, H. J.; Chandler, M. A. (2008). "Pliocene role in assessing future climate impacts" Eos. 89 (49): 501–502 http://adsabs.harvard.edu/abs/2008EOSTr..89..501R

[2] Ogburn S 2013, “Ice-Free Arctic in Pliocene, Last Time CO2 Levels above 400 PPM”, Nature Magazine, May 10, 2013 https://www.scientificamerican.com/article/ice-free-arctic-in-pliocene-last-time-co2-levels-above-400ppm/

[3] Dwyer, G. S.; Chandler, M. A. (2009). "Mid-Pliocene sea level and continental ice volume based on coupled benthic Mg/Ca palaeotemperatures and oxygen isotopes" (PDF). Philosophical Transactions of the Royal Society A. 367 (1886): 157–168 https://web.archive.org/web/20111021024807/http://pubs.giss.nasa.gov/docs/2009/2009_Dwyer_Chandler.pdf

[4] IPPC 2001 Climate Change 2001: Synthesis Report https://www.ipcc.ch/ipccreports/tar/vol4/011.htm

[5] Tokarska K et al 2016 The climate response to five trillion tonnes of carbon Nature Climate Change volume 6, pages 851–855 (2016) https://www.nature.com/articles/nclimate3036

[6] Stern N 2016 “The roles of financial institutions and finance ministries in delivering the Paris Agreement on climate change” http://www.lse.ac.uk/GranthamInstitute/news/the-roles-of-financial-institutions-and-finance-ministries-in-delivering-the-paris-agreement-on-climate-change/

[8] GSI 2016 Global Sustainable Investment Review http://www.gsi-alliance.org/wp-content/uploads/2017/03/GSIR_Review2016.F.pdf

[9] Byrd J & Cooperman E 2016 “Shareholder Activism for Stranded Asset Risk:An Analysis of Investor Reactions for Fossil Fuel Companies” Business School, University of Colorado Denver https://corporate-sustainability.org/wp-content/uploads/Shareholder-Activism.pdf

[10] https://rhg.com/research/the-hidden-cause-of-americas-coal-collapse/

[11] Bloomberg New Energy Finance 2018 “Electric Vehicle Outlook 2018” https://about.bnef.com/electric-vehicle-outlook/#toc-download

[12] https://www.carbontracker.org/reports/mind-the-gap/

[13] SSE 2016 Report on Progress http://unctad.org/en/PublicationsLibrary/unctad_sse_2016d1.pdf

[14] PRI 2017 “What rating agencies are doing on ESG factors” https://www.unpri.org/fixed-income/what-rating-agencies-are-doing-on-esg-factors/81.article

[15] See “CBI Data for GGFI 2” at https://www.finance-watch.org/ggfi-global-green-finance-index/

[17] http://www.sseinitiative.org/

[19] BOE 2017 The Bank of England’s response to climate change Quarterly Bulletin, 2017 Q2 https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2017/the-banks-response-to-climate-change.pdf?

[21] Dombret, A. & Loriet, A. 2017 “These are the risks and opportunities of Green Finance” WEF https://www.weforum.org/agenda/2017/07/green-finance-risk-and-opportunity/

[22] OCI 2017 “Talk Is Cheap: How G20 Governments are Financing Climate Disaster” http://priceofoil.org/content/uploads/2017/07/talk_is_cheap_G20_report_July2017.pdf