The Impact Of Covid-19 On “A Tale Of Two Middle Classes”

Monday, 11 May 2020By Patricia Lustig & Gill Ringland

In an earlier Pamphleteer contribution, ‘A Tale of Two Middle Classes’, we posed a question. The headlines at the time suggested that the middle class in Asia was becoming an economic force to be reckoned with, while the middle class in the northern, mature economies was hollowing out. The question was, ‘Why?’

We concluded that the rise of the middle class in Asia is largely due to the economic activity of Asians, manufacturing and selling goods and services to industries and consumers largely in Asia. The age profile in many parts of Asia (but not all - China, Korea and Japan are over this bulge) meant that large numbers of young people were entering the growing workforce, setting up new households and buying furnishings and consumer goods. This is driving demand and creating new industries.

Many of these young people had migrated to, or had families who already lived in, urban areas. This move is linked with smaller family sizes and higher female literacy. So, more and more people aspired to and attained Levels 3 and 4 (see below) in these economies, increasing the numbers of consumers (i.e. people who are able to buy goods and services).

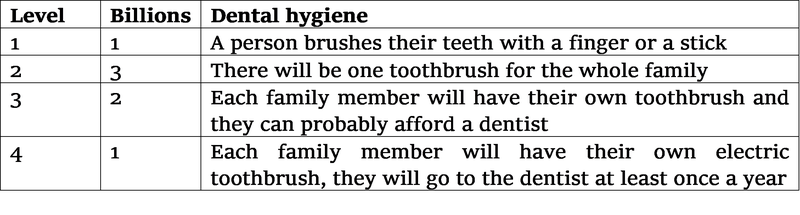

We used the UN terminology popularised by Hans Rosling as Levels 1, 2, 3 and 4, for people’s living standards. A quick aide memoire for the living standards of each Level is:

Levels 3 and 4 are often referred to as ‘middle class’. When we wrote the article in August 2018, there were about 3 billion “middle class” globally.

Once people have a Level 3 lifestyle, they start to travel for fun – maybe as well as for work. Initially in country and then when they reach a Level 4 income, internationally. First by motorbike or train, thereafter, often by private car or air. Purchasing insurance and financial services and becoming interested in pollution and protecting the environment is also characteristic of Levels 3 and 4.

A differentiating factor between the evolving Asian economies vs mature economies is the rate of innovation. As we illustrate in Lustig & Ringland (2018)1, the research activity and patents filed in key areas, such as artificial intelligence, by China are now in the same league as those from the USA.

In financial services, platforms such as Alibaba are bringing financial empowerment to people in new ways. And, in evolving economies people were more likely to think that the world was getting better.

Two factors are starkly different in mature economies:

- Demographics of little or no growth in the workforce, a static or declining and aging population with increasing dependency factors, means that the traditional drivers of employment – new household formation – are largely absent. People may switch their spending to personal services and travel, but these industries do not often provide Level 4 incomes for most employees.

- The long period of stability and growth since WWII has meant that many instruments of investment and innovation seem to have lost their focus, and the innovation pipeline has decayed, with the impact on patents etc. in key areas as described above. An older population may also be more conservative and less open to new ideas, meaning a potentially less helpful home market for innovation.

The Impact Of Covid-19?

Countries have handled the pandemic differently, with very diverse rates of infection and deaths. However, evidence is growing that this pandemic will lead to a severe world-wide depression2.

The immediate impact of the covid-19 pandemic on the middle class in mature economies may well be positive, in increasing focus on the resilience of health and emergency services, with an increase in the number and perceived value of public sector jobs. However, the lockdown of countries is reducing the incomes of professional services economies that export their expertise – many from mature to Asian economies – decimating Level 3 and 4 incomes. In the longer term, the devastation of the global economy will be the most important factor.

A recent ILO report3 finds that epidemics and economic crises can trigger worsening inequality. Based on past experience and current information on the Covid19 pandemic, and insights from previous crises, there a number of groups that can be identified which suffer economically from pandemics. These are: young and old workers (who are more likely to suffer un- and under-employment), hospitality and care services workers (predominantly women), and gig and migrant workers.

It could be that many people in these groups in Asia had recently achieved Level 3 incomes and are now facing a return to Level 2 or worse - Travel and Tourism contribute about 10% to global GDP4 and the loss of tourist income will hit people at Levels 2 and 3 disproportionately.

Globally, the depression of economies and shrinkage of incomes will affect everybody. People with middle class incomes on the whole have more cushion to deal with immediate fallout – the exception may be those recently entering the middle class in Asia.

In summary, the middle class in mature economies may lose comparative wealth through to 2040, compared particularly with the middle class in Asia, due to underlying economic fundamentals. However, it is unlikely to shrink in numbers.

The middle class in Asia has a higher proportion of people recently joining Level 3 and 4. They may have less of a safety net, and numbers will shrink as result of the pandemic. The global economic effect of the loss of the purchasing power of a significant proportion of the middle class in Asia could be one of the most serious fallouts from the covid-19 pandemic for the next decade.

www.global-megatrends.com

References

1 Lustig, P and Ringland, G., Megatrends and How to Survive Them: preparing for 2032, Cambridge Scholars Publishing, October 2018. See www.lasa-insight.com for more information.

2 https://www.project-syndicate.org/commentary/white-swan-risks-2020-by-nouriel-roubini-2020-02

3 https://www.ilo.org/global/topics/coronavirus/impacts-and-responses/WCMS_739047/lang--en/index.htm

4 https://www.statista.com/statistics/1099933/travel-and-tourism-share-of-gdp/