Burning Rembrandts

Monday, 30 September 2019By Simon Mills

This article is an extract from the fourth edition of the Global Green Finance Index, the world's most comprehensive review of the green finance performance of financial centres. Further details can be found at https://www.longfinance.net/programmes/financial-centre-futures/global-green-finance-index/

Biodiversity is the net diversity of living organisms in all habitats including terrestrial, marine, and other aquatic ecosystems and the ecological complexes of which they are part; this includes diversity within species, between species, and of ecosystems. Biodiversity forms the foundation of the vast array of ecosystem services, such as flood protection, waste decomposition and food production that support human well-being and economic systems.

Ecosystem services are complex and highly interdependent (see box 1). However, a defining and sometimes problematic feature of current economic models is the concept that some forms of natural capital can be substituted by other goods and services which perform similar functions1, for example, livestock or fish farming replacing hunting or fishing as a source of calories.

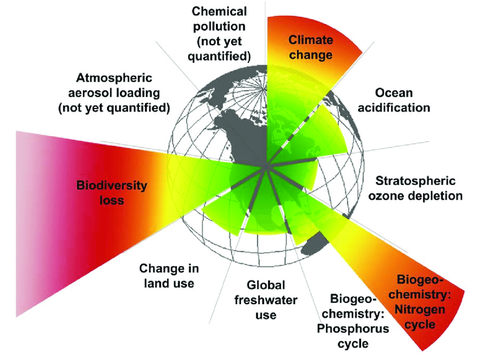

Substitution is not without cost. In 2009, the Stockholm Resilience Centre brought together 29 leading Earth-system scientists, who identified a set of nine critical Earth-system processes with biophysical thresholds, or ‘tipping points’, called ‘Planetary Boundaries’. Crossing these boundaries will lead to irreversible environmental change, undermining the ‘safe space for human development’.

Three of them have already been crossed: biosphere integrity, climate change and biogeochemical cycle (nitrogen and phosphorus cycles), whilst ocean acidification is entering the danger zone.

Figure 1 | Planetary Boundaries2

There is a growing awareness that environmental degradation is causing biodiversity, and the ecosystems supported by it, to reach breaking point. Recent reports by the IPCC and IPBES[3] leave little doubt: the combination of climate change and the depletion of biodiversity and ecosystems puts societys on the path to environmental collapse.

The last few years have seen a plethora of reports charting the havoc being wrought on the planet:

- 40 per cent of insect species, the bedrock of eco-systems, face extinction4

- Huge numbers of plant species, crucial for food and pharmaceuticals, are going extinct5

- The UN is alarmed that plant diversity in farmers’ fields is decreasing, that nearly a third of fish populations are overfished, and a third of freshwater fish species assessed are considered threatened 6

- Driven by acidification and rocketing temperatures, marine species are going extinct even faster than those on land7

- Forest areas are predicted to decline by 13 per cent by 2030, mostly in South Asia and Africa8, although there is also concern at the rapid surge in deforestation currently occurring in Brazil9

The public is becoming alarmed at the scale and pace of the threats facing the planet. From an increase in vegetarian and veganism to campaigns against fast fashion and plastic packaging, both businesses and politicians are coming under increasing pressure to address environmental issues as policy priorities.

Complacent, Indifferent Or Enabler? The Role Of Financial Systems And Services In The Destruction And Protection Of Biodiversity

Unlike heavy industry, the most significant impacts of the financial services sector on biodiversity and natural capital are not associated with direct resource consumption or the emission of pollutants or greenhouse gases by individual financial services firms. Impacts arise from the enabling role that these organisations play in providing capital for infrastructure or activities that direct society down pathways that are unsustainable.

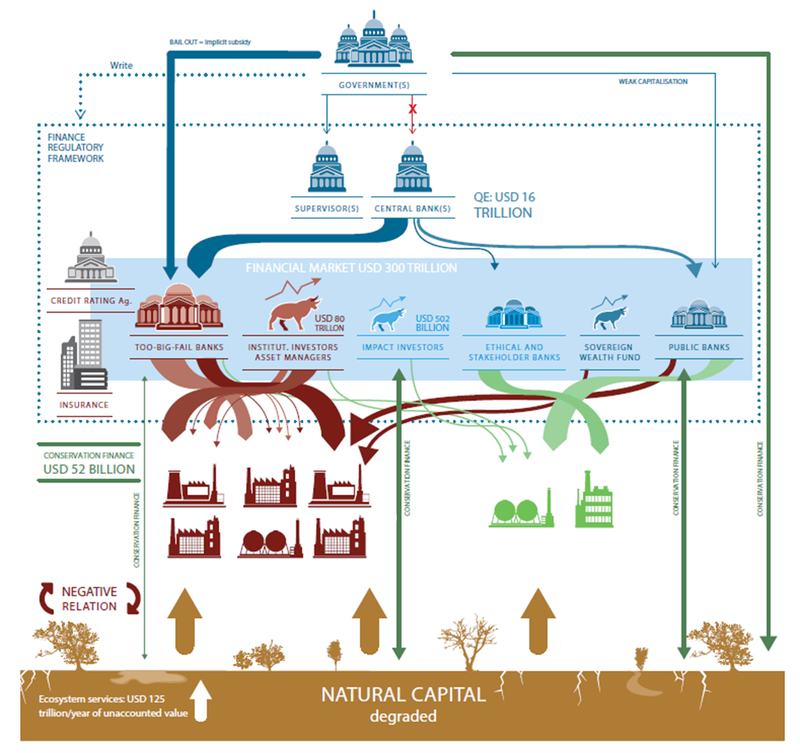

The risk of environmental collapse, resulting from natural capital depletion, can be described as a systemic risk because of the complex interdependence and interconnectedness between the elements of ecosystems; and also financially systemic, because the financial system shares similar characteristics and risks of contagion. The ability of the financial system to harm the ecosystems on which it depends raises questions about whether the financial sector has the right mix of institutions to meet environmental goals. As Figure 2 illustrates, the quantities of finance being made available for fossil fuel and other unsustainable activities are far larger that the amounts directed to sustainable activities, and private banks and institutional investors are far more dominant than the impact investors, stakeholder banks, sovereign wealth funds and public banks that are likely to have sustainability at the core of their missions.

Figure 2 | Finance Ignoring Nature

Source: Finance Watch 2019

The root cause of the issue is linked to short-term horizons for risk and reward, and a failure to deal effectively with externalities. These challenges, as pointed out in Mainelli and Gifford’s 2009 paper The Road To Long Finance: A Systems View of the Credit Scrunch10, already pose significant risks to the global financial system, and, according to many commentators11, have not been addressed effectively in the decade since the financial crisis occurred.

There is an urgent need to assess risks at the macro-economic level. Central banks and supervisory authorities are responsible for mapping these risks, modelling their interactions with economic and financial systems, and taking steps to mitigate them.

Private financial institutions are driven by a simple ‘risk/return’ ratio, and shifting capital involves changing this ratio. There is, therefore, a need, first, to enhance the financial sector’s understanding of risks related to natural capital depletion and, second, to amend the return expected from activities they invest in by showing the hidden costs of economic activities and internalizing these negative externalities in the production cost. If investing in environmentally harmful activities leads to lower returns and more risk than sustainable activity, financial institutions will automatically shift their investment.

But the players in the financial system find it difficult to see, think and act long term, when structural characteristics incentivise short-term returns. As private finance is currently ill-suited to conservation finance, there is a need to address this issue at three levels:

- Firstly, to address market failures at a macro-economic level by extending time horizons and internalising externalities. As Mainelli and Gifford (2009) state, “Wicked problems, [problems which are difficult or impossible to solve because of incomplete, contradictory, and changing requirements that are often difficult to recognize] cannot be solved by larger government intervention, but equally, we cannot just sit back and wait for the free market to save the day. What may be needed is bolder, yet more pointed, government intervention.”

- Secondly, finance from ‘mission-oriented’ financial institutions must be unlocked: that is, financial institutions which do not follow a logic only of profit, but also answer to a public interest mission (public and development banks), or to social and environmental criteria (ethical banks and impact investors).

- Finally, the value of ecosystem services and biodiversity must be recognised through the development of mainstream financial products such as loans, bonds or equities (see table 1), which derive income streams from the protection and sustainable exploitation of biodiversity and ecosystems.

Economic System Reliance On Ecosystems

Natural capital can be defined as the world’s stocks of natural assets which include geology, soil, air, water and all living things12. Natural capital yields ecosystem services, such as energy (fuel), calories (food) and raw materials, as well as providing homeostatic functions such as climate regulation and flood control. These ecosystem services are often closely interlinked, so that over-exploitation or poor stewardship in one area may have detrimental effects in another.

Managing costs and ensuring long-term value creation across supply chains requires businesses to understand better their dependencies on biodiversity and ecosystem services, and to integrate these considerations into long-term business strategies, risk-management approaches and other business activities13.

From an investor perspective, the profitability and long-term survival of some sectors depends on well-functioning ecosystems, notably agriculture, fisheries and pharmaceuticals. The last of these sectors is especially reliant on biodiversity, as “nature, the master of craftsman of molecules, provides the bedrock resource for drug development, novel chemotypes and pharmacophores, and scaffolds for amplification into efficacious drugs for a multitude of diseases and other valuable bioactive agents”14.

Systemic failures by the financial system to value biodiversity and ecosystem services have long been recognised. In 1999, Forest Trends (a trans-national NGO), launched the Katoomba Initiative – an international working group dedicated to advancing markets and payments for ecosystem services – including watershed protection, biodiversity habitat, and carbon sequestration.

During the conference of the parties (COP) to the Convention on Biological Diversity (CBD) in Nagoya in 2010, world governments agreed to a strategic plan for biodiversity conservation, including the 20 Aichi Biodiversity Targets (ABT) to be met by 2020. Assuming that public finance would not be made available for conservation at sufficient scale, the CBD’s strategic plan for 2011-2020 placed much emphasis on innovative financial mechanisms to help stimulate private investment, such as payments for ecosystem services, biodiversity offsets, markets for green products, etc.

The financing needed to implement the 20 Aichi targets (widely denounced as too modest to avert a crisis), was estimated in the range $150 to $440 billion per year. Yet even this has not been achieved.

Even with innovative market machanisms, few conservation projects are bankable: most have low revenues, low rates of return, and relatively high transaction costs. Only around USD 50 billion of conservation finance is being raised annually15, a sixth of the estimated global funding need. And of this, 80 per cent comes not from financial markets but from public and philanthropic sources.

The CBD’s Conference of the Parties is expected to update its strategic plan at the 15th COP in Beijing in October 2020.

Valuing Nature

At the heart of humankind’s problematic relationship with the planet is how we value nature and natural services.

For much of human existence, nature was an elemental force to be tamed, with enclaves of civilization carved out of a threatening wilderness. Once humanity entered the Anthropocene (a theoretical geological epoch, marking indelible human impact on geology and natural systems, and defined as starting either with widespread agriculture or the industrial revolution) philosophers and scientists have been concerned at the damage humans were having on the natural world, and by extension, themselves.

Functioning ecosystems are essential to life on earth, yet economics and society at large either fails to place any value on natural capital or focuses on individual species without taking account of the systems which they are part of.

Placing a value on nature is fundamentally problematic. We may be able to place a commercial value on a human kidney, and live doners can earn life-changing sums of money in some jurisdictions by selling one, but no one would be willing to sell their heart or liver. Likewise, we may be able to place a commercial value on a tree, but what realistic price can be placed on a forest, the flood protection and pollution amelioration it provides, the as yet undiscovered medicines that are locked in its biodiversity and the mental well-being it provides.

As the political philosopher Michael J. Sandel said in his 2012 Atlantic article16 "Economists often assume that markets are inert, that they do not affect the goods being exchanged. But this is untrue. Markets leave their mark. Sometimes, market values crowd out nonmarket values worth caring about."

Just as there are difficulties in valuing nature’s benefits, so there are difficulties valuing the costs to nature of environmentally harmful activities. In a study for UNPRI, Trucost estimated the global costs associated with the environmental impact of the operations of the largest 3,000 companies in the world, to be in the order of US$2.15 trillion17. This analysis, however, acknowledged limitations in relation to global data availability for natural resources, other than fisheries and timber, as well as for environmental impacts such as water pollution, heavy metals, land-use change and waste, particularly in non-OECD countries. Moreover, Trucost stressed the fact that its results could be significantly higher if methodological and data obstacles could be overcome in order to account for ecosystem services degradation (e.g. climate regulation).

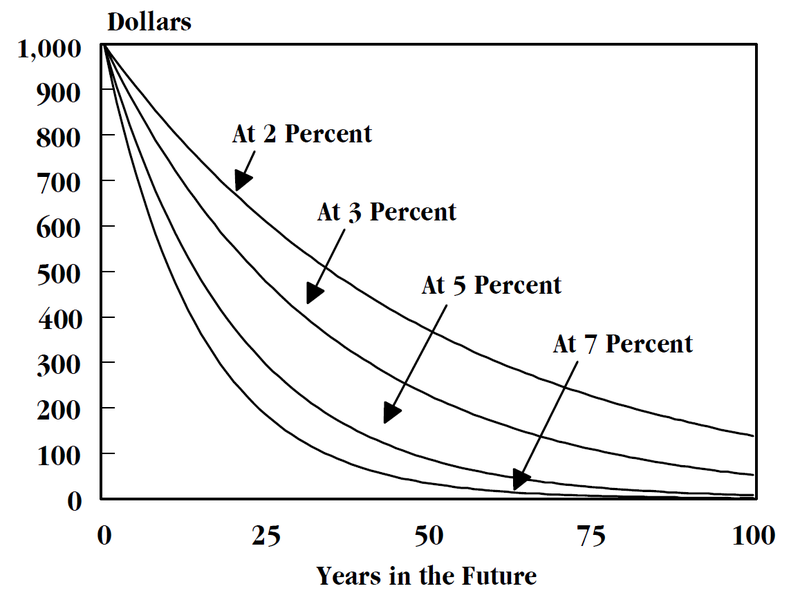

At present these costs are borne by society as a whole, not by industry and shareholders and this situation is compounded by the fact that markets do not value conservation, only consumption – so an endangered rhino is worth more as an aphrodisiac or hunting trophy than as a living animal. The discounting of assets (see figure 3), which is standard accountancy practice, may be useful for investors assessing the timing of financial returns but is highly problematic for decisions about conservation and sustainability.

Figure 3 | Curves Representing Constant Discount Rates Of 2%, 3%, 5%, And 7%

Source: Congressional Budget Office18

As Jeffery Sachs points out19 we are subject to the “tyranny of the present over the future”, particularly when the rate of interest diminishes the incentive for the resource owner to harvest the resource at a sustainable rate and a natural asset discounts to zero over the span of a few decades, whilst a forest or a whale can take a century to reach maturity.

Challenges To Positive Action

Several key challenges present themselves in harnessing the power of markets to protect biodiversity:

- Externalities And Income – classical economic theory imbues biodiversity with some of the properties of a public good: individuals cannot (or should not) be excluded from consuming a particular commodity (for example, the flood protection qualities of upland forests), and available supply is more or less independent of the number of consumers20. These properties drive the “Tragedy of the Commons”.

- Who benefits? – many of the issues fundamental to the protection of species lie in the hands of the communities where those resources exist. Unfortunately, custom and culture are rarely a match for economic necessity, and unless there are substantial direct economic and social benefits for communities associated with the conservation of species and habitats, over-exploitation is inevitable. Deriving sustainable income streams from biodiversity, and the ecosystems and habitats which support it, is extremely challenging.

- Metrics And Data -whilst the concept of biodiversity is well established, its measurement has yet to be pinned down in the same way that carbon emissions have been established as the unit of measurement for climate change impact assessments21. Calculations to derive diversity and species richness were first developed by Robert MacArthur and Edward O. Wilson in 196722. The results of their, and subsequent formulae designed to measure natural systems, require interpretation and are ill-suited to the needs of the financial services sector. As Z/Yen highlighted in its 2011 report for the NERC, without standardised metrics, it is more difficult to measure and compare the performance of financial instruments designed to promote biodiversity and protect biodiversity and ecosystem services23.

Awareness Amongst Financial Service Professionals

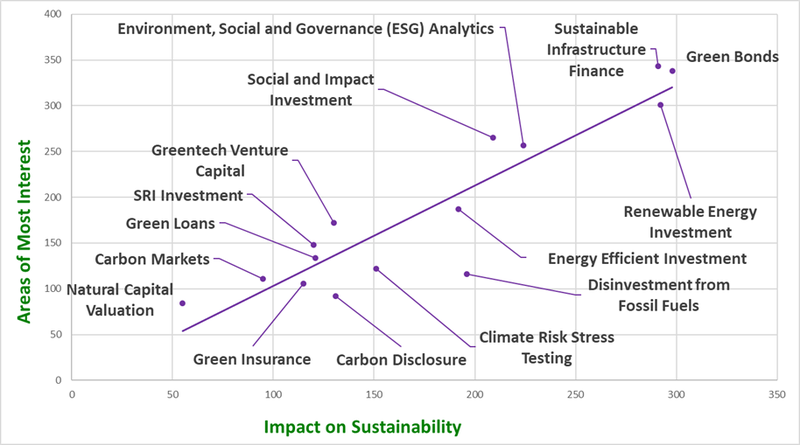

For each issue of the Global Green Finance Index, practitioners have been asked to identify the areas that they consider to be of most interest to them, and the areas they consider to have the greatest impact on sustainable development. Despite the high potential impact of biodiversity loss on economic and financial system stability, the valuation of natural capital (and by extension biodiversity) has consistently ranked very low (see figure 4).

In part this may be a result of the issues discussed in the previous section. However, it is also likely to be a result of the shortage of tradable financial products which have a focus on this issue.

Figure 4 | The Views of Financial Services Professionals On Green Financial Products And Services

Connecting Finance With Nature

There is growing recognition that environmental aspects, including biodiversity and ecosystem service-related ones, have a material impact on investment risks and returns. Driven by increasing awareness of the positive impact of sustainable business practices on long-term profitability, the business and financial services sectors have come to recognise the importance of a sustainable environment.

Initiatives such as UN Principles for Responsible Investment or UNEP Finance Initiative are illustrative of efforts to demonstrate and further explore the relationship between environmental, social and governance issues and financial performance.

Many investors active in socially responsible investment (SRI), particularly pension funds and other institutional investors, are taking a growing interest in the environmental, social and governance (ESG) aspects related to their investments, including environmental issues such as climate change, water scarcity and biodiversity.

From 2012 to October 2018, assets managed in accordance with environmental, social and governance (ESG) principles increased 60%, to reach $1.05 trillion24. The first six months of 2019 saw record €36.9bn transferred into sustainable funds in Europe, and this pattern is being repeated across the globe. ESG criteria are becoming standard in credit analysis: Standard & Poor’s, Moody’s and Fitch Ratings now include ESG factors in their rating decisions.

These risks have a serious systemic dimension. The loss of biodiversity and interruption of ecosystem services is a material risk for the financial system – certainly in the long-term, even in the short-term for some investments/sectors – and needs to be included in stress tests by institutions and their supervisors. Macro-prudential instruments should be used to penalize nature-depleting investments where relevant.

Policy makers have already indicated that a regulatory response will be needed although, so far, no firm commitments have been proposed. The Network for Greening the Financial System (NGFS), a group of central bankers and financial supervisors set up to address financial system concerns linked to climate change, wrote in April 2019 that “there are compelling reasons why the NGFS should also look at environmental risks relevant to the financial system. For instance, environmental degradation could cascade to risks for financial institutions, as reduced availability of fresh water or a lack of biodiversity could limit the operations of businesses in a specific region. These could turn into drivers of financial risks and affect financial institutions’ exposures to those businesses.”25

This suggests that regulatory action will be forthcoming. In the meantime, the destruction of biodiversity and ecosystems is continuing to accelerate.

Three paths are essential for financial services to connect with biodiversity:

Firstly, effective reporting of the impacts of investment decisions on biodiversity in order to ensure that investors and fund managers are aware of the potential biodiversity risks associated with investment decision making.

Tools are already available to enable this to happen such as:

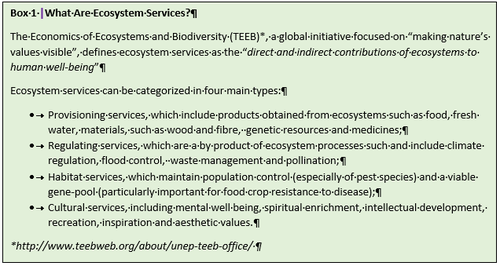

- UNEP’s The Economics of Ecosystems and Biodiversity (TEEB) programme26. TEEB is a global initiative focused on “making nature’s values visible”. Its principal objective is to mainstream the values of biodiversity and ecosystem services into decision-making.

- InVEST (Integrated Valuation of Ecosystem Services and Tradeoffs)27 is a suite of models developed by Stanford University used to map and value the goods and services from nature that sustain and fulfil human life.

What is required, as with reporting on other sustainability risks (particularly those associated with climate change), is intervention by regulators to mandate effective reporting, such as confidence accounting28, for listed companies.

Secondly, the phasing out of environmentally-harmful subsidies (EHS) which encourage the depletion of biodiversity and damage ecosystems, particularly with respect to forestry, agriculture and fisheries. The European Union (EU) has committed to remove or phase out environmentally harmful subsidies29, the EU and other nations and economic areas have a long way to go to ensure that EHS are removed.

Finally, the flow of private finance into ecosystem service and biodiversity protection must be encouraged. Over the last few decades, conservation projects which aim to protect or enhance biodiversity have primarily been funded from public and philanthropic sources. As public finances have come under strain, conservation organisations have been under pressure to diversify their funding strategies.

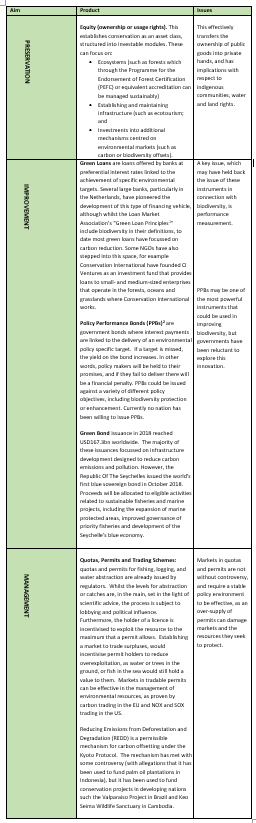

One solution they have sought is “Impact Investment” - private capital invested with the specific intention of achieving a measurable or environmental impact alongside financial returns. Impact investment designed to meet an environmental goal is sometimes referred to as conservation finance. The feat of overcoming the ‘tragedy of the commons, and unlocking the value of ecosystems is made possible using a number of financial products tailored for specific purposes (see table 1).

Table 1| Financial Products Supporting Biodiversity

Leadership

Biodiversity projects have been part of firms’ corporate social responsibility toolkit for decades, and organisations such as HSBC have done excellent work with international conservation foundations such as IUCN and WWF32. However, this type of work, although extremely worthwhile, does not address the systemic threats facing global biodiversity which arise from unsustainable development patterns.

Biodiversity still has low recognition amongst financial services professionals, and although societal awareness of the threats facing ecosystems is growing, it still has only a marginal impact on the consciousness of financial service organisations.

Momentum does appear to be growing though, and awareness of biodiversity issues is beginning to penetrate investment analysis, where risks arising from new legislation, breaching of quotas, fines and third-party claims, usage rights, suspension of permits or licences, refusals to grant licences, legal proceedings (particularly around major developments) are prompting analysts to take taking firms’ biodiversity management into account in valuations and estimates of future profitability, particularly in the SRI sector.

UNEPFI’s Biodiversity Principles Recommendations for the Financial Sector33, published in 2011, have begun to have an impact; ASN Bank from The Netherlands has put biodiversity at the heart of its corporate plans, with the target that all investments and loans of ASN Bank result in a positive effect on biodiversity in 203034.

Unlocking Forest Finance (UFF)35 brings together NGOs, environmental and social sector safeguarding institutes, financial sector experts and strategic advisors including Credit Suisse, the European Investment Bank and Althelia Ecosphere in order to catalyse the creation of new financial mechanisms to stop the conversion of tropical forest for commodity production, and to support a shift towards more sustainable modes of development.

These initiatives are still small scale and are dwarfed by the flow of finance into unsustainable activity, but indicate a shift in awareness and understanding at the margins.

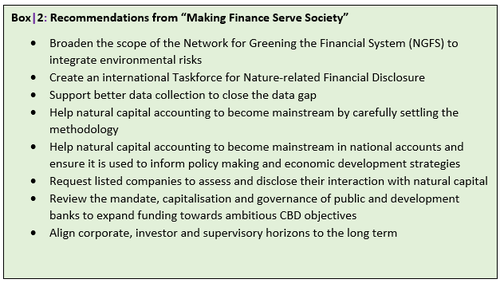

As Finance Watch has argued in a recent report (see Box 2),36 while there is much that can be done to help private finance address biodiversity loss, the scale of the problem will also require a substantial public investment plan, using a range of mission-oriented financial institutions and tools, including monetary policy, to transform systems of production and consumption as well as crowding-in more private funds.

Conclusions

Awareness of biodiversity risk within the financial services sector is still at an extremely low level. Macro-economic systems, regulation, and classical economic theory continue to drive unsustainable growth patterns.

Markets can be a powerful force for good, but they require direction and parallel, complementary initiatives in the public sector.

The damage that society continues to inflict on biodiversity, and the ecosystems which support it, arise from economic activity that fails to take account of externalities. Reducing this damage will require:

- Significant intervention by regulators in order to internalise costs into decision-making;

- Effective metrics to measure performance;

- A combination of private and public finance

- Realisation that ecosystems do not exist in isolation, and that unlocking the value of nature requires that the rights and interests of indigenous populations must be harnessed in the protection of biodiversity.

Acknowledgement

This supplement builds on the work done by Finance Watch in their 2019 report “Making Finance Serve Nature From The Niche Of Conservation Finance To The Mainstreaming Of Natural Capital Approaches In Financial Systems”

References

[1] Carpenter S 1997 Towards Refined Indicators Of Sustainable Development, Phil & Tech 2:2 Winter 1997 Georgia Institute of Technology

[2] Figgis P et al 2015 Valuing Nature: Protected Areas and Ecosystem Services, Australian Committee for IUCN Isbn: 978-0-9871654-5-9

[3] Intergovernmental Panel on Climate Change (IPCC), Summary for Policymakers of IPCC Special Report on Global Warming of 1.5°C approved by governments, October 2018; Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES), Global Assessment of Biodiversity and Ecosystem Services, May 2019

[4] Sánchez-Bayoa F & Wyckhuysbcd K 2019 Worldwide Decline Of The Entomofauna: A Review Of Its Drivers Biological Conservation Volume 232, April 2019, Pages 8-27

[5] Humphreys A, Govaerts R, Ficinski S, Lughadha E & Vorontsova M 2019 Global Dataset Shows Geography And Life Form Predict Modern Plant Extinction And Rediscovery Nature Ecology & Evolution, Vol 3, July 2019, 1043–1047

[6] FAO, The State of the World’s Biodiversity for Food and Agriculture, 2019, 576p.

[7] Pinsky M, Eikeset A, McCauley D, Payne J & Sunday J 2019 Greater Vulnerability To Warming Of Marine Versus Terrestrial Ectotherms Nature, Vol 569 2 May 2019

[8] OECD 2008 Environmental Outlook to 2030, 2008

[10] Mainelli M & Gifford B 2010 The Road to Long Finance: A Systems View of the Credit Scrunch https://www.zyen.com/media/documents/Road_to_Long_Finance.pdf

[11] IMF 2018 A Decade after the Global Financial Crisis: Are We Safer? https://www.imf.org/en/Publications/GFSR/Issues/2018/09/25/Global-Financial-Stability-Report-October-2018

[12] World Forum On Natural Capital https://naturalcapitalforum.com/about/

[13] OECD 2019 Biodiversity: Finance and the Economic and Business Case for Action https://www.oecd.org/environment/resources/biodiversity/G7-report-Biodiversity-Finance-and-the-Economic-and-Business-Case-for-Action.pdf

[14] Veeresham C 2012 Natural Products Derived From Plants As A Source Of Drugs Journal Of Advanced Pharmaceutical Technology & Research 2012 Oct-Dec; 3(4): 200–201 https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3560124/

[15] Finance Watch 2019 Making Finance Serve Naturehttps://www.finance-watch.org/publication/making-finance-serve-nature-report/

[16] Michael J. Sandel 2012 What Isn't For Sale?, The Atlantic https://www.theatlantic.com/magazine/archive/2012/04/what-isnt-for-sale/308902/

[17] Trucost 2010 Universal Ownership: Why Environmental Externalities Matter To Institutional Investors https://www.unpri.org/environmental-issues/universal-ownership-why-environmental-externalities-matter-to-institutional-investors/4068.article

[18] US Congress 2003 The Economics of Climate Change: a Primer https://www.cbo.gov/sites/default/files/108th-congress-2003-2004/reports/04-25-climatechange.pdf

[19] Sachs, G 2008, Common Wealth: Economics For A Crowded Planet, Penguin (Allen Lane)

[20] Wiesmeth H. (2012) Public Goods in Environmental Economics. In: Environmental Economics. Springer Texts in Business and Economics. Springer, Berlin, Heidelberg

[21] Mainelli M & Harris I 2011 The Price Of Fish p285 Nicholas Brealey ISBN 978-1-85788-571-2

[22] MacArthur R and Wilson E O 1967 The Theory of Island Biogeography Princeton University Press (Revised edition 26 Feb. 2001) ISBN-10: 0691088365

[23] Z/Yen 2011 Finance, Biodiversity And Managed Ecosystems: Where’s The Data? https://www.zyen.com/media/documents/nerc_biodiversity_2011.pdf

[24] GSIA 2018 Global Sustainable Investment Review http://www.gsi-alliance.org/wp-content/uploads/2019/06/GSIR_Review2018F.pdf

[25] NGFS, First comprehensive report, “A call for action Climate change as a source of financial risk”, April 2019, https://www.dnb.nl/binaries/NGFS%20Call%20for%20action%20report_tcm46-383435.pdf

[26] TEEB http://www.teebweb.org/about/unep-teeb-office/

[27] InVest https://naturalcapitalproject.stanford.edu/invest/

[28] Mainelli M & Mills S 2017 Financial Innovations and Sustainable Development https://www.longfinance.net/media/documents/BSDC_report.pdf

[29] IEEP 2012 Study Supporting The Phasing Out Of Environmentally Harmful Subsidies https://www.cbd.int/financial/fiscalenviron/eu-studyehs.pdf

[30] LMA 2018 Green Loan Principles https://www.lma.eu.com/application/files/9115/4452/5458/741_LM_Green_Loan_Principles_Booklet_V8.pdf

[31] Mainelli M 2019 Policy Performance Bonds For ESG & Climate Change – A Primer https://www.longfinance.net/news/pamphleteers/beyond-words-why-london-climate-week-needs-policy-performance-bonds/

[32] WWF 2017 Five Years Five River Basins: Funding Freshwater Conservation Through The HSBC Water Programme https://www.wwf.org.uk/sites/default/files/2017-06/170324_HWP-five-years-five-rivers.pdf

[33] UNEPFI & VfU 2011 Biodiversity Principles – Recommendations For The Financial Sector https://www.unepfi.org/fileadmin/documents/biodiversity_principles_en.pdf

[34] https://www.asnbank.nl/over-asn-bank/duurzaamheid/biodiversiteit/biodiversity-in-2030.html

[35] https://www.globalcanopy.org/what-we-do/financing-sustainable-landscapes/unlocking-forest-finance

[36] Finance Watch 2019 Making Finance Serve Nature https://www.finance-watch.org/publication/making-finance-serve-nature-report/